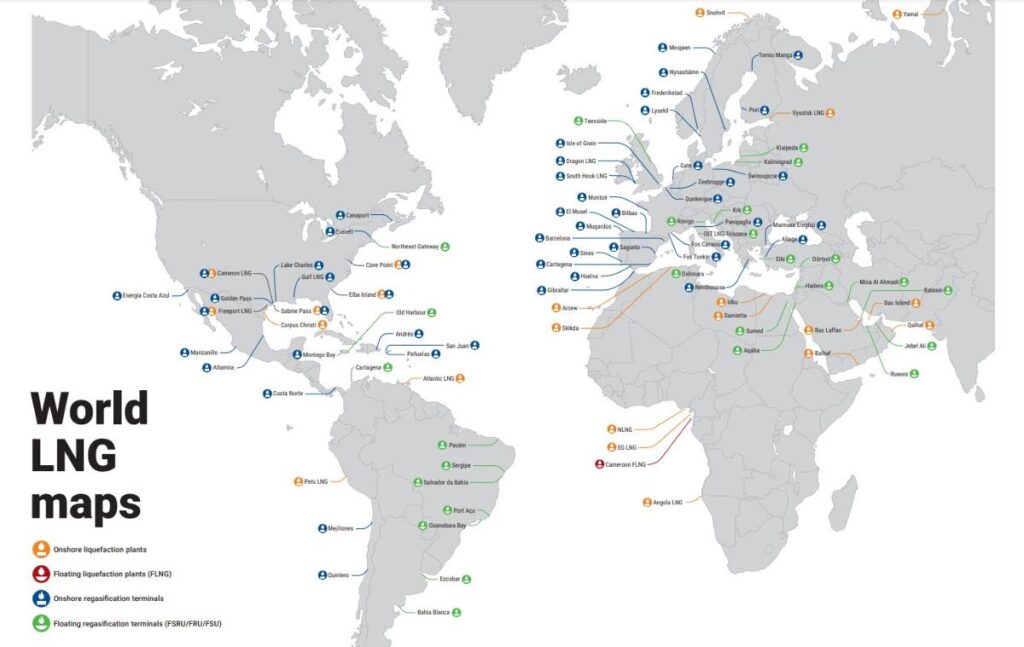

(TT Geological Society, 20.Jan.2022) — Natural gas and by extension liquefied natural gas (LNG) have become forerunners in the hydrocarbon industry.

The reputation of being a cheap, clean and an abundant fuel source more environmentally friendly than oil and coal has made it quite attractive amid renewable energy alternatives that are not as affordable now.

With increasing supply demands along with mounting pressures to become carbon emissions net zero by the year 2050, it is clear to see natural gas and LNG has solidified its importance in the global energy demand for the long-term future. It forms an integral role in the fuel security strategies of many countries as the transition fuel and preferred energy source towards the goal of sustainable renewable energy.

With natural gas and LNG maintaining prices at the highest recorded in history at over US$4/mmbtu, the complexity of supply and demand along with the latest developments of the US becoming a major exporter instead of importer, have posed some significant challenges and opportunities for Trinidad and Tobago in the wake of the evolving LNG markets.

Our vast natural gas reserves and developed LNG infrastructure with years of proven expertise puts TT in a strategic position to pivot in this energy demand transition. With most untapped reserves situated in deep-water technically challenging plays and recent bid rounds failing to attract the much-needed interests of IOCs, gas shortages will persist and continue to affect the major downstream industries in coming years.

Effects of the gas shortage have already been felt by Atlantic LNG and Methanol Holdings scaling back activity. Steel giant Mittal has already left due to unfavourable conditions and labour force.

Increased domestic consumptions of LNG and natural gas from the governments ambitious carbon reducing initiatives such as 22 CNG stations with respective 17,000 vehicle conversions along with expanding downstream higher value chain industries will be deciding factors further contributing to supply shortfalls.

A new guaranteed gas allocation policy may be implemented by the government for power generation to the petrochemical industry using natural gas and LNG which will entice investors into producing high value products such as methanol, urea and ammonia amongst others.

There are upcoming projects pending approval in 2022 as highlighted by the Ministry of Energy and Energy Industries (MOEEI) with the potential to add some growth with the Cassia Compression and Matapal projects from bpTT but without upstream developments will have production declines in a few years.

Additionally, Shell signed an agreement in late 2021 with MOEEI to develop the Loran-Manatee field in the East Coast Marine Area – a controversial cross border gas field with Venezuela which TT has agreed to develop on its own side without Venezuela.

The Dragon gas deal in northwest Trinidad, also a Shell project, has been suspended indefinitely due to US sanctions against Venezuela further jeopardising much needed natural gas supplies.

Latest additions from DeNovo Energy, Touchstone Exploration, Trinity Oil and Challenger Energy group will all be insufficient to maintain Atlantic LNG’s trains, but it fills some existing supply deficits.

Both Shell and bpTT with renewed contracts for train one until 2024 re-negotiated their existing contracts for attractive E&P development to realise supplies to train one which are currently lacking.

Opportunities to capitalise can include to increase investor incentives to introduce favourable fiscal terms and attractive licences agreements. Review of the taxation regime also needs to be addressed.

The changes in the supplemental petroleum tax though favourable are not enough to offset the changes of operations being less profitable overall. The oil and gas specific tax regime is governed by the Petroleum Taxes Act, an outdated framework relatively unchanged since its inception in 1969. In an attempt to update the Petroleum Taxes Act to benefit the nation it inadvertently deferred investment potential and opportunities.

Further threats of LNG technological advancements throughout the entire value chain and increased competition from new LNG players globally are also looming.

TT LNG pricing benchmarked against crude oil have left us vulnerable to the volatility of oil price fluctuations incurring losses when oil price is low. NGC usually negotiates long term supply contracts on gas prices below current global and future market values.

The government has indicated it will be reviewing existing contracts. This gives rise to the possibility of unfavourable investor terms and uncertainty driving away investment potential for NGC.

The market has become more competitive with increasing preference being shown towards shorter term five year and under contracts. Spot pricing by physical exchange at hubs allows for variables such as production levels, gas storage injections and withdrawals, weather patterns, pricing and availability of competing energy sources, and the market participants’ views of future trends in any of these or other variables to affect pricing.

The energy minister has indicated that LNG cargoes were often re-routed to the more competitive Latin American market as opposed to the US which at one point was the single largest importer of LNG from NGC with its integrated model.

As the US has now ventured into the export category being relatively new, TT can have the advantage of securing long term supply contracts within the Caribbean and Latin America utilising its diplomatic ties and new accessibility of markets through the Panama Canal like Chile in a shorter and more economical turn-around time.

This logic also holds true the Asian markets with the world’s largest gas consumers which lack pipeline access for natural gas. They are more concerned with long term security of supplies rather than competitiveness and utilises similar pricing strategies as NGC benchmarked against crude oil.

There is competition from platform LNG (PLNG): liquefaction facilities are being built onto existing platforms instead of the ships. Ship-to-ship transfers, floating storage and liquefaction facilities (FLNG), floating storage and regasification units (FSRU) and larger capacity modern LNG ships reducing burn-offs and loss of LNG in transit is making LNG more accessible and easily transported. It is allowing the remote development of offshore reserves, directly at production platforms eliminating costly pipeline infrastructure to a port facility.

Small scale LNG (SSLNG) facilities are also becoming popular for those smaller operators with lack of upfront capital investment for large scale facilities. The SSLNG can then be increased or expanded with cash flow availability over time.

The acceleration or delay of infrastructure will play a crucial role in the future of supply and demand dynamics of LNG and the survivability of TT’s LNG and natural gas sector.

____________________