(WoodMac, 23.Feb.2023) — Ukraine’s battle is existential. The country has suffered a year of lost lives, its people forced to live each day in perpetual fear and witness the destruction of homes, communities and infrastructure. Millions have fled the country. Russia’s war has had a huge impact outside Ukraine, too, […]

Tag: Russia

Enhancing the US-UK Sanctions Partnership

(US Treasury, 17.Oct.2022) — As Directors of two of the world’s leading financial sanctions implementation authorities, we are committed to our close working relationship. As a testament to this ongoing commitment, on Thursday, 13 October 2022, OFAC and OFSI concluded a multi-day technical exchange in London between our two offices. […]

Russia/Ukraine Conflict Could Hurt Trinidad and Tobago in Long Term

(Trinidad and Tobago Newsday, 23.Feb.2022) — War! What is it good for? Apparently it’s good for oil, gas and petrochemical prices. For the past few weeks concerns over Russia’s aggressive stance against Ukraine have contributed in part to the daily increase in oil, gas and ammonia prices. Foreign Affairs Minister […]

Venezuela Producing Around 450,000 b/d

(Energy Analytics Institute, 1.Dec.2020) — Venezuela is said to be producing around 450,000 barrels per day and exporting more with the assistance of Chinese and Russians companies lifting the South American country’s oil. Production could rise to at least 600,000 b/d in coming months, oil union official Ivan Freites told […]

Venezuela’s Maduro doubling down on earnings from illicit means

HOUSTON, TEXAS (Ian Silverman and Piero Stewart, Energy Analytics Institute, 13.Aug.2020, Words: 966) — Venezuela’s President Nicolas Maduro is doubling down on earning money through illicit means where sanctions have less of an impact while also doubling down on alliances with autocratic regimes whether its Cuba, Iran, Russia or others, […]

Sisi Wins Approval For Possible Libya Intervention

(Reuters, 20.Jul.2020) — Egypt’s parliament gave President Abdel-Fattah al-Sisi the green light for possible military intervention in Libya by approving the deployment of armed forces abroad to fight “terrorist groups” and “militias”. A sharp military escalation in Libya, where fighters led by eastern commander Khalifa Haftar have been battling the […]

Investors In Russian Pipeline At Risk Of US Sanctions

(Reuters, 15.Jul.2020) — U.S. Secretary of State Mike Pompeo on Wednesday warned investors in two Russian natural gas pipeline projects that they could face sanctions as the Trump administration seeks to curb the Kremlin’s economic leverage over Europe and Turkey. Pompeo told a news conference that European investors in the […]

US Swaps Venezuelan Fuel Oil For Russian Products

(Oilprice.com, 13.Jul.2020) — The United States has been raising its imports of fuel oil from Russia over the past year and a half after the U.S. imposed sanctions on Venezuela’s exports, Reuters reported on Monday, quoting data from Refinitiv Eikon. Venezuela’s heavy crude oil is suitable to process in complex […]

Russia Backs Venezuela In Fight Against US

(Newsweek, 24.Jun.2020) — Russia vowed to support Venezuela in its campaign to counter U.S.-backed regime change after the Pentagon sailed warships nearby in the Caribbean to challenge the Latin American country. On Wednesday, Russian Foreign Minister Sergey Lavrov called Venezuela his country’s “reliable friend both in Latin America and in […]

Mexico To Sit Out Extension Of OPEC+ Oil Output Cuts

(Reuters, 6.Jun.2020) — Mexico will not join other top oil producers in extending through July output cuts aimed at propping up the price of crude, Energy Minister Rocio Nahle said on Saturday. Made up of OPEC members and allies led by Russia, the group known as OPEC+ agreed in April […]

OPEC+ To Meet Saturday On Extending Cuts

(Reuters, 5.Jun.2020) — OPEC and its allies led by Russia will meet on Saturday to discuss extending record oil production cuts and to push laggards such as Iraq and Nigeria to comply with existing curbs. The producers known as OPEC+ previously agreed to cut supply by 9.7 million barrels per […]

US Sanctions Four Firms For Transporting Venezuelan Oil

(Aljazeera, 2.Jun.2020) — The United States Treasury Department on Tuesday said it had sanctioned four shipping firms for transporting Venezuelan oil, the latest escalation in Washington’s effort to depose socialist President Nicolas Maduro by cutting off the OPEC nation’s crude exports. Marshall Islands-based Afranav Maritime Ltd, Adamant Maritime Ltd and […]

US Senators Expected To Sanction Nord Stream 2

(Reuters, 29.May.2020) — Two U.S. senators are expected to introduce next week sanctions on the Nord Stream 2 natural gas pipeline that Russia is trying to finish, but which Washington has opposed since the Obama era, a source familiar with the matter said on Friday. The sanctions, which would have […]

Iran’s 4th Fuel Tanker Nears Venezuelan Waters

(Fars News Agency, 28.May.2020) — Iran’s fourth tanker full of gasoline has entered the Caribbean and is close to the Venezuelan territorial waters. Venezuelan armed forces are due to escort the tanker, Faxon, en route to its destination, as in the case of its three predecessors. The five-tanker Iranian-flagged flotilla […]

Mexico To Remain In Opec+, No Output Cuts Planned

(Argus, 22.May.2020) — Mexico will remain within the Opec + group but has no plans for further production cuts, the energy ministry told Argus today. “Mexico will participate in the Opec + meeting in June but we do not contemplate implementing more cuts,” the ministry said. “There are no plans […]

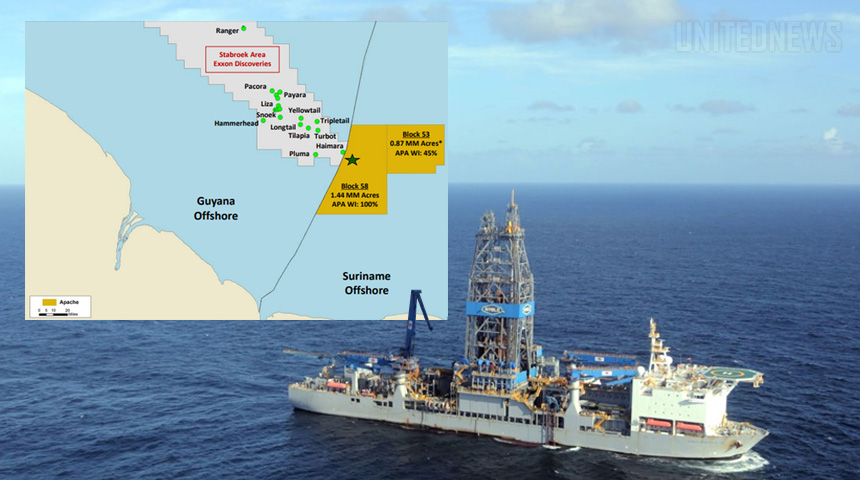

The Only Hotspot Where Big Oil Will Still Spend

(Oilprice.com, 7.May.2020) — Oil majors may be slashing spending and deferring development plans across the globe, but they remain committed to developing the newest offshore oil finds in the heart of Latin America. The oil price collapse has forced the world’s oil companies to slash spending and curb production at […]

Venezuela Floats Lean PdV With Russia Unit

(Argus, 27.Apr.2020) — The two Maduro loyalists who have been effectively running Venezuela’s national oil industry for two months were officially appointed today as acting heads of the oil ministry and PdV, with a mandate to dismantle the company’s bloated Chavez-era organization in favor of a lean structure featuring a […]

Saudi OSPs For Oil Exports Bode Well For Asian Refiners

(WoodMac, 16.Apr.2020) — On 13 April, Saudi Arabia announced the Official Selling Prices (OSPs) for its May crude oil exports. The new OSPs speak volumes about Saudi Arabia’s crude export strategy after agreeing to cut production in the OPEC+ deal on 10 April 2020. Wood Mackenzie research director Sushant Gupta […]

OPEC And Non-OPEC To Cut Output By 9.7 MMb/d

(OPEC, 12.Apr.2020) — The 10th (Extraordinary) OPEC and non-OPEC Ministerial Meeting was held via videoconference, on Sunday, 12 April 2020, under the Chairmanship of HRH Prince Abdul Aziz Bin Salman, Saudi Arabia’s Minister of Energy, and co-Chair HE Alexander Novak, Minister of Energy of the Russian Federation. The Meeting reaffirmed […]

Collapsing Demand Sets Terms In OPEC+ Battle

(WoodMac, 9.Apr.2020) — Since OPEC+’s failure to agree on production restraint on 5-6 March, the implications of the Covid-19 pandemic have become far clearer, sparking a crisis in the oil market as prices fell and supply ramped up. The problem for these producers is the scale of the fall in […]

‘Dead Cow’ Oil Play Set To Be Next Permian Is Now Dead

(Bloomberg, 1.Apr.2020) — Just a bit more than 3 weeks ago, the head of Argentina’s state-run driller outlined an aggressive $1.8 billion spending plan for 2020 in the country’s Vaca Muerta shale region, based on $60-a-barrel crude. With global prices starting the year above $68, it wasn’t unrealistic. Now, all […]

Maduro Highlights Need To Stabilize Oil Market

(Energy Analytics Institute, Piero Stewart, 31.Mar.2020) — Venezuela’s President Nicolás Maduro highlighted the importance of the agreements between the Organization of Petroleum Exporting Countries (OPEC) and its allies (OPEC+), as well as the need to advance in rapprochements between the organization, Russia and Saudi Arabia. “I proposed the need to […]

Kremlin Fights US Sanctions, Backs Maduro

(Bloomberg, 30.Mar.2020) — The Kremlin’s sudden shift of ownership of multi-billion-dollar oil projects in Venezuela shields oil giant Rosneft PJSC from further U.S. sanctions but keeps Moscow firmly behind embattled President Nicolas Maduro amid a wider stand-off with Washington. “Russia is not walking away from Maduro and will seek to […]

Venezuela’s Oil Output Falls To Five-month Low

(Reuters, 30.Mar.2020) — Venezuela’s crude production ended last week at around 670,000 barrels per day (bpd), according to documents seen by Reuters and two people with access to output data, the lowest level in five months amid U.S. sanctions and falling global demand. The Orinoco oil belt, Venezuela’s largest producing […]

Rosneft’s Venezuelan Oil Loads Cancelled – Data

(Reuters, 28.Mar.2020) — Three large crude carriers (VLCCs) chartered by units of Russian oil major Rosneft to transport Venezuelan oil left Caribbean waters empty on Saturday after the cargoes were cancelled due to sanctions, according to Refinitiv Eikon data and a document from Venezuelan state-run oil firm PDVSA. The vessels […]

Rosneft To Sell Venezuela Operations To Russian Gov’t

(S&P Global Platts, 28.Mar.2020) — Russia’s largest crude producer Rosneft said Saturday it is ceasing operations in Venezuela and selling all assets related to activities there. “Today [Saturday], Rosneft entered into an agreement with a company 100%-owned by the Russian government on the sale of shares and termination of its […]

Rosneft Sells Its Venezuelan Assets

(Rosneft, 28.Mar.2020) — Rosneft announces the termination of its operations in Venezuela and the disposal of its assets, related to operating in Venezuela. Today Rosneft concluded an agreement with the company 100% owned by the Government of Russian Federation, to sell all of its interest and cease participation in its […]

Which Supply Is Most At Risk Of Shut-in?

(WoodMac, 27.Mar.2020) — The coronavirus pandemic is reducing oil demand. The OPEC+ production restraint agreement fell apart on 6 March and Saudi Arabia is rapidly increasing supply. The result: Brent crude has plunged to less than US$30/bbl. This will have a significant impact on currently producing fields and future supply. […]

US Targets Maduro Regime With Fresh Charges

(WSJ, 22.Mar.2020) — The U.S. quietly unsealed criminal cases against two former officials at Venezuela’s state oil monopoly this month as part of what American officials say is a new round of charges and sanctions against a Maduro government they accuse of systemic corruption, narcotrafficking and stealing billions of dollars […]

Maduro Suggests OPEC, OPEC+ Discuss Oil Market

(Energy Analytics Institute, Piero Stewart, 12.Mar.2020) — Venezuela’s President Nicolas Maduro has suggested that members of OPEC and OPEC+ return to discussions about balancing the oil market. “Let us seek agreements to provide short-term, medium-term and long-term solutions that will restore the oil markets to an equilibrium point,” state oil […]

Venezuela Discussing Oil Prices With OPEC, Russia

(TASS, 12.Mar.2020) — Venezuelan authorities are discussing the situation with the oil price collapse with OPEC and Russia, President Nicolas Maduro said on Thursday at a press conference broadcasted in Twitter. “We contacted our partners in OPEC, such our partners as Russia, with oil producing countries, to undertake steps in […]

China “Teapot” Refiners Crank Up Run Rates

(Reuters, 11.Mar.2020) — China’s independent oil refiners are cranking up production as local governments begin to relax strict measures to contain the coronavirus and fuel demand begins to recover. A sharp plunge in crude oil markets triggered by the erupting Saudi-Russia price war has also boosted profit margins. Also known […]

Mexico Says Hedge Covers Oil Income

(Reuters, 10.Mar.2020) — Mexico’s finance minister said on Tuesday a $1.4 billion hedge program completely covered 2020 national oil income following a steep drop in crude prices, adding the government needed to accelerate spending to help stimulate a flagging economy. The oil hedging program, the world’s largest financial oil deal, […]

Venezuela Cause Drifting Off International Agenda

(Argus, 10.Mar.2020) — Venezuela’s US-backed opposition is scrambling to stay relevant at home and abroad as the US and other foreign patrons turn inward to focus on slowing the spread of coronavirus and mitigating the economic fallout of an oil price collapse. In a bid to reinvigorate his movement, Juan […]

PetroMonagas Incorporates Turbo Generator

(Energy Analytics Institute, Piero Stewart, 20.Feb.2020) — In order to generate its own electricity, the PetroMonagas joint venture incorporated use of an electric turbo generator (TG2) at its upgrader at the José Antonio Anzoátegui Industrial Complex located in the northern part of Anzoátegui state. With incorporation of the generator, the […]

Maduro Shakes Up PDVSA Amid Oil Sector Emergency

(Bloomberg, 19.Feb.2020) — Venezuela’s President Nicolas Maduro declared an “energy emergency” as he announced a commission to revamp state oil company Petroleos de Venezuela SA, redoubling efforts to shore up the nation’s crumbling oil industry. Economy Vice President Tareck El Aissami will lead the commission, which will focus on boosting […]

Rosneft Says US Sanctions On RTSA Illegal

(Rosneft, 18.Feb.2020) — The sanctions announced by the U.S. Treasury Department against Rosneft’s subsidiary RTSA and its Chairman are illegal, unjustified, and an act of legal abuse. Rosneft has been implementing its projects in Venezuela in strict compliance with rules of international and national laws. In the course of the […]

Ending Putin’s Support Of Venezuela Not Easy For US

(AP, 18.Feb.2020) — In October 2016, the head of Russia’s largest oil company traveled to the birthplace of Hugo Chávez, in the empty, sweltering plains of Venezuela, to unveil a giant bronze statue of the late socialist leader that he and his longtime friend, Russian President Vladimir Putin, commissioned from […]

US Imports Of Russian Residue Complicate Venezuela Sanctions

(Argus, 10.Feb.2020) — US Gulf Coast refiners have been increasing their imports of a crude oil residue from Russia in response to both sanctions on Venezuelan crude exports and declining prices of high sulfur fuel oil ahead of International Maritime Organization’s revamp of marine fuel sulfur regulations. The trend could […]

Beyond The Dragon Deal

(Trinidad Newsday, 5.Feb.2020) — One of the biggest lessons we can take away from the pausing of the landmark cross-border agreement between TT and Venezuela is how our interests are inherently wrapped up with international politics. Prime Minister Dr Keith Rowley’s confirmation on Monday that US sanctions have had an […]

Russia Sends Lavrov To Venezuela

(Reuters, 4.Feb.2020) — Russian Foreign Minister Sergei Lavrov will visit Venezuela on Friday in a show of support for President Nicolas Maduro, a socialist who Washington wants out of power. Russia has helped Maduro weather a political crisis as the United States has targeted Caracas with sanctions and, like dozens […]

Venezuela Weighs Privatizing Oil

(Bloomberg, 27.Jan.2020) — Facing economic collapse and painful sanctions, the socialist government of Venezuelan President Nicolas Maduro has proposed giving majority shares and control of its oil industry to big international corporations, a move that would forsake decades of state monopoly. Maduro’s representatives have held talks with Russia’s Rosneft PJSC, […]

Guaido Rubbing Elbows In Surprise Foreign Trip

(Argus, 20.Jan.2020) — The US government is hoping a high-profile international tour by Venezuelan opposition leader Juan Guaido will re-inject momentum into its protracted campaign to unseat President Nicolas Maduro. Guaido turned up in Colombia today in the initial leg of his first journey outside Venezuela since an ill-fated February […]

Oil Is The Only Way Back Up For Venezuela

(Oilprice.com, 19.Jan.2020) — There’s only one path to rebuilding Venezuela, and it’s paved with oil. For the time being, that path leads nowhere. The key to controlling everything now lies with the National Assembly, the only body with the power to hand out oil licenses—and Maduro’s recent scheme to retake […]

China Scaling Back Economic Support For Maduro: Envoy

(Reuters, 15.Jan.2020) — The Trump administration’s envoy on Venezuela said China appears to be scaling back economic support for President Nicolas Maduro, and Beijing acknowledged a diminishing role largely due to U.S. sanctions against the OPEC nation. As China’s economic activities have declined, Maduro and his socialist government are becoming […]

Abrams Sees China Scaling Back Support For Maduro

(Reuters, 15.Jan.2020) — The Trump administration’s envoy on Venezuela said China appears to be scaling back economic support for President Nicolas Maduro, and Beijing acknowledged a diminishing role largely due to U.S. sanctions against the OPEC nation. As China’s economic activities have declined, Maduro and his socialist government are becoming […]

Venezuelan Oil Exports Fell By A Third In 2019

(Reuters, 7.Jan.2020) — Venezuela’s oil exports plummeted 32% last year to 1.001 million barrels per day, according to Refinitiv Eikon data and state-run PDVSA’s reports, as a lack of staff and capital drove output to its lowest level in almost 75 years and U.S. sanctions shrank exports markets. The drop […]

US Considering More Venezuela Sanctions

(S&P Global Platts, 6.Jan.2020) — The US may respond to escalating political disarray in Venezuela by allowing a sanctions waiver for Chevron and four US oil services companies to expire later this month and could ratchet up oil sanctions on foreign companies still working in the South American country, analysts […]

PDVSA Cedes Oilfield Operations To Foreign Firms

(Reuters, 3.Jan.2020) — Venezuelan state company PDVSA is letting some joint venture partners take over the day-to-day operation of oilfields as its own capacity dwindles due to sanctions and a lack of cash and staff, according to a former oil minister, an opposition lawmaker and industry sources. Crude production by […]

Venezuela Is Quietly Ramping Up Oil Production

(Oilprice.com, 31.Dec.2019) — If anyone is to ever write a guidebook on political survival, the skills of Venezuelan President Nicolás Maduro would certainly top the contemporary charts. This autumn went relatively well for the besieged leader as the political headlines drifted towards the US-China trade wars, OPEC+ production cuts and […]