(Argus, 20.Dec.2019) — PdV is leaning on joint-venture partners as it looks to continue a nascent crude output revival and live up to an improved economic outlook for 2020

The US sanctions-hit government of Venezuelan president Nicolas Maduro aims to turn a corner in its struggle to maintain power, as state-owned PdV tries a new strategy to revive output and dollarisation eases the country’s financial woes.

PdV is promoting new and revamped joint ventures — mainly with domestic partners — to restore oil output to 1.5mn-2mn b/d in 2020. Among the new ventures is PetroSur, in which PdV subsidiary CVP will partner Cyprus-based Inversiones Petroleras Iberoamericanas (IPI) to develop the Orinoco belt’s Junin 10 block, which holds estimated extra-heavy crude reserves of 1.03bn bl. IPI’s chief partners include former chairman and chief executive of Spanish firm Repsol, Alfonso Cortina, former Repsol legal affairs adviser Ramon Blanco Balin and Venezuelan investor Alejandro Betancourt, the senior partner at privately owned Venezuelan energy contractor Derwick Associates. The firm will make an initial payment of $400mn to PdV for Junin 10 rights. The block was assigned in 2010 to a PdV joint venture with Chinese state-owned CNPC, but CNPC withdrew in 2014 after PdV failed to meet its share of investment.

PdV is working on another upstream partnership in eastern Venezuela, where its minority shareholder in the dormant PetroDelta project proposes spending $800mn over three years to produce 100,000 b/d of heavy crude in exchange for full operational control and marketing rights. The 40pc stakeholder in PetroDelta is Venezuelan-Italian consortium CT Energy, whose top executives are Venezuelan telecommunications magnate Oswaldo Cisneros and Panama-based Element Capital Advisors president Francisco D’Agostino, also Venezuelan.

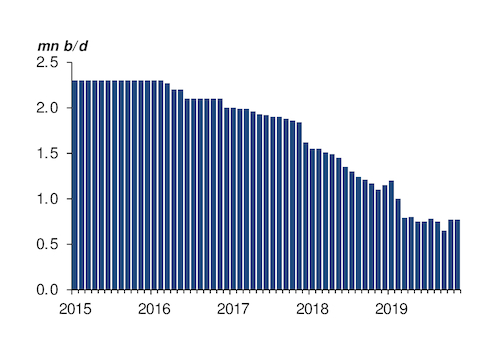

The planned changes have not been communicatedto the opposition-controlled national assembly, which has a constitutional mandate to approve all oil joint ventures. But Venezuela’s oil production has in any case rebounded in recent months, to 770,000 b/d in November from 650,000 b/d in September, Argus estimates (see chart). And PdV crude output has rebounded to over 800,000 b/d in recent weeks, partly by quietly transferring operational and procurement controls to PdV’s minority joint-venture partners, including Russia’s state-controlled Rosneft, CNPC and Repsol, although fresh investment is still on hold.

Greenback mounting

US sanctions imposed on PdV in January constricted oil revenues that historically accounted for up to 90pc of Venezuela’s income. And while they have failed to dislodge Maduro, they have compelled his government to ease economic controls this year, modestly improving the country’s 2020 economic outlook. Maduro’s biggest economic achievement this year has been to curb hyperinflation. National assembly advisers estimate inflation in January-November at over 5,500pc, compared with the central bank’s 2018 estimate of 130,000pc.

And falling oil revenues have forced Maduro to phase out most domestic price controls and loosen capital controls in a bid to encourage foreign investment and facilitate remittances from Venezuelans abroad. Remittances are expected to jump to about $6bn next year, up from an estimated $4bn this year. This would be equivalent to almost 80pc of the central bank’s hard currency reserves of $7.5bn. The trends are driving a robust black market in dollars and euros.

Dollarisation is a necessary “pressure release valve” that is allowing private-sector companies to secure hard currency to finance imports, Maduro said in October, adding “thank God for dollarisation”. Venezuelan business chamber Fedecamaras says that this year, for the first time in decades, the private sector will account for up to 25pc of GDP, and probably more in 2020.

***