(FMC, 9.Feb.2021) — FMC Corporation reported fourth quarter 2020 results that were in-line with the company’s updated outlook from 19 January 2021.

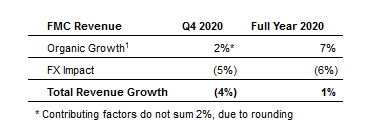

Fourth quarter revenue was approximately $1.15bn, a decrease of 4% versus fourth quarter 2019. Excluding the impact of foreign currencies, sales grew 2% organically year over year.

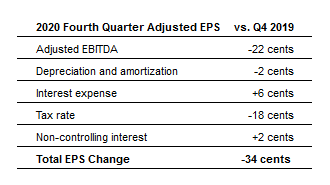

On a GAAP basis, the company reported earnings of $0.38 per diluted share in the fourth quarter, compared to a loss of $0.02 per diluted share in the fourth quarter 2019. Adjusted earnings were $1.42 per diluted share, a decrease of 19 percent versus fourth quarter 2019.

Fourth Quarter 2020 Highlights

— Revenue of $1.15bn, down 4% versus Q4 2019, up 2% organically1

— GAAP net income of $47mn, versus a loss of $3 million in Q4 2019

— Adjusted EBITDA of $290mn, down 9% versus Q4 2019

— GAAP earnings of $0.38 per diluted share, versus a loss of $0.02 per diluted share in Q4 2019

— Adjusted earnings per diluted share of $1.42, down 19% versus Q4 2019

Full-Year 2020 Highlights

— Revenue of $4.64bn, reflecting 1% growth and 7% organic growth1

— GAAP net income of $551mn, up 15% versus 2019

— Adjusted EBITDA of $1.25bn, up 2% versus 2019

— GAAP earnings of $4.22 per diluted share, up 17% versus 2019

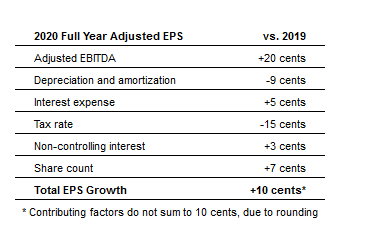

— Adjusted earnings per diluted share of $6.19, up 2% versus 2019

— GAAP cash flow from operations of $737mn, up 33% versus 2019

— Free cash flow of $544mn, up 80% versus 2019

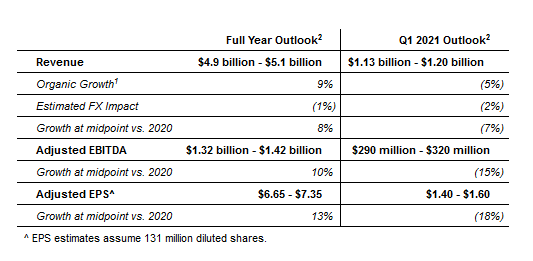

Full-Year 2021 Outlook2

— Revenue in the range of $4.9 to $5.1bn, reflecting 8% growth at the midpoint versus 2020

— Adjusted EBITDA in the range of $1.32 to $1.42bn, reflecting 10% growth at the midpoint versus 2020

— 2021 adjusted earnings are expected to be in the range of $6.65 to $7.35 per diluted share, reflecting 13 percent growth at the midpoint versus 2020, excluding any impact from 2021 share repurchases

— Free cash flow is expected to be in the range of $530 to $620mn, reflecting 6 percent growth at the midpoint versus 2020

— Company expects to repurchase $400 to $500mn of FMC shares in 2021, beginning in Q1

Mark Douglas, FMC president and CEO said: “While our fourth quarter performance was impacted heavily by external factors, some of which are expected to persist into the first quarter of 2021, we posted solid full-year 2020 results and grew the business in a very challenging economic environment.”

The revenue decrease was driven by a 5% FX headwind and a 3% volume decrease, partially offset by a 4% increase in pricing. Strong volume growth in EMEA and Asia was more than offset by weakness in North America and Latin America. Sales in EMEA increased 45% year over year, due to a particularly strong quarter for our diamide insecticides and cereal herbicides in addition to significant pre-ordering in the UK in advance of Brexit. In Asia, revenue increased 11% year over year, driven by broad volume growth in India, China, Japan and Australia. In North America, sales decreased 34% year over year. The majority of this decline was due to supply chain disruptions, including COVID-related factors associated with logistics and a U.S.-based tolling partner. The remainder of the decrease was due to reduced volume in lower-value pre-emergent herbicides. Latin America sales decreased 9% year over year but grew 4% excluding significant FX headwinds. In addition to the headwind from foreign currency, Brazil sales were lower than forecasted due to severe drought that delayed the start of the season and persisted throughout the fourth quarter, resulting in fewer application days. In Argentina, substantial product inventory located in bonded warehouses was not released by customs officials in a timely manner.

For the full year, FMC reported revenue of $4.64bn, an increase of 1% compared to 2019. Excluding the impact of foreign exchange, year-over-year sales grew 7% organically. On a GAAP basis, the company reported full-year earnings of $551mn, or $4.22 per diluted share, which represent year-over-year increases of 15% and 17%, respectively. Full-year adjusted earnings were $6.19 per diluted share, an increase of 2% compared to the prior year.

On a GAAP basis, cash flow from operations was $737mn, an increase of 33% versus 2019. Free cash flow in 2020 was $544mn, an increase of 80% versus 2019. Better than expected working capital performance and lower capital additions, combined with timing of one-time items, more than offset lower than expected adjusted EBITDA.

2021 Outlook2

The company is forecasting full-year 2021 revenue to be in the range of $4.9bn to $5.1bn, driven by growth in all regions and representing an 8 percent increase at the midpoint versus 2020. The revenue growth will be driven primarily by volume, with price increases expected to more than offset FX headwinds. Full-year adjusted EBITDA is expected to be in the range of $1.32bn to $1.42bn, representing 10% year-over-year growth at the midpoint. 2021 adjusted earnings are expected to be in the range of $6.65 to $7.35 per diluted share, representing a year-over-year increase of 13% at the midpoint, excluding any impact from 2021 share repurchases. Full-year earnings growth drivers include strong volume growth led by Asia, Latin America and North America. Price increases in all regions except Asia are forecast to outweigh FX at the earnings level. Full-year free cash flow is expected to be $530 to $620mn, representing a 6% increase year-over-year. The company expects to repurchase $400 to $500mn of FMC shares in 2021, beginning in the first quarter.

“Looking ahead at 2021, we see an improved ag macro environment, and we expect to deliver strong revenue and earnings growth, once again driven by the strength of our portfolio and our balanced geographic and crop exposure. Our projected 2021 growth rates keep us firmly on track to deliver our 5-year growth targets of 5 to 7% revenue and 7 to 9% adjusted EBITDA compounded annual growth for 2018 through 2023,” said Douglas.

First Quarter 2021 Outlook2

First quarter revenue is expected to be in the range of $1.13bn to $1.20bn, representing a 7% decrease at the midpoint compared to first quarter 2020, and a 5% decline excluding foreign currency headwinds. This decline is driven by a cotton acreage reduction in Brazil, the timing of Brexit-related sales in Q4 2020 and continued portfolio changes related to discontinued registrations in EMEA. Adjusted EBITDA is forecast to be in the range of $290mn to $320mn, representing a 15% decrease at the midpoint versus Q1 2020. FMC expects adjusted earnings per diluted share to be in the range of $1.40 to $1.60 in the first quarter, a decrease of 18% at the midpoint.

Tale 4

____________________