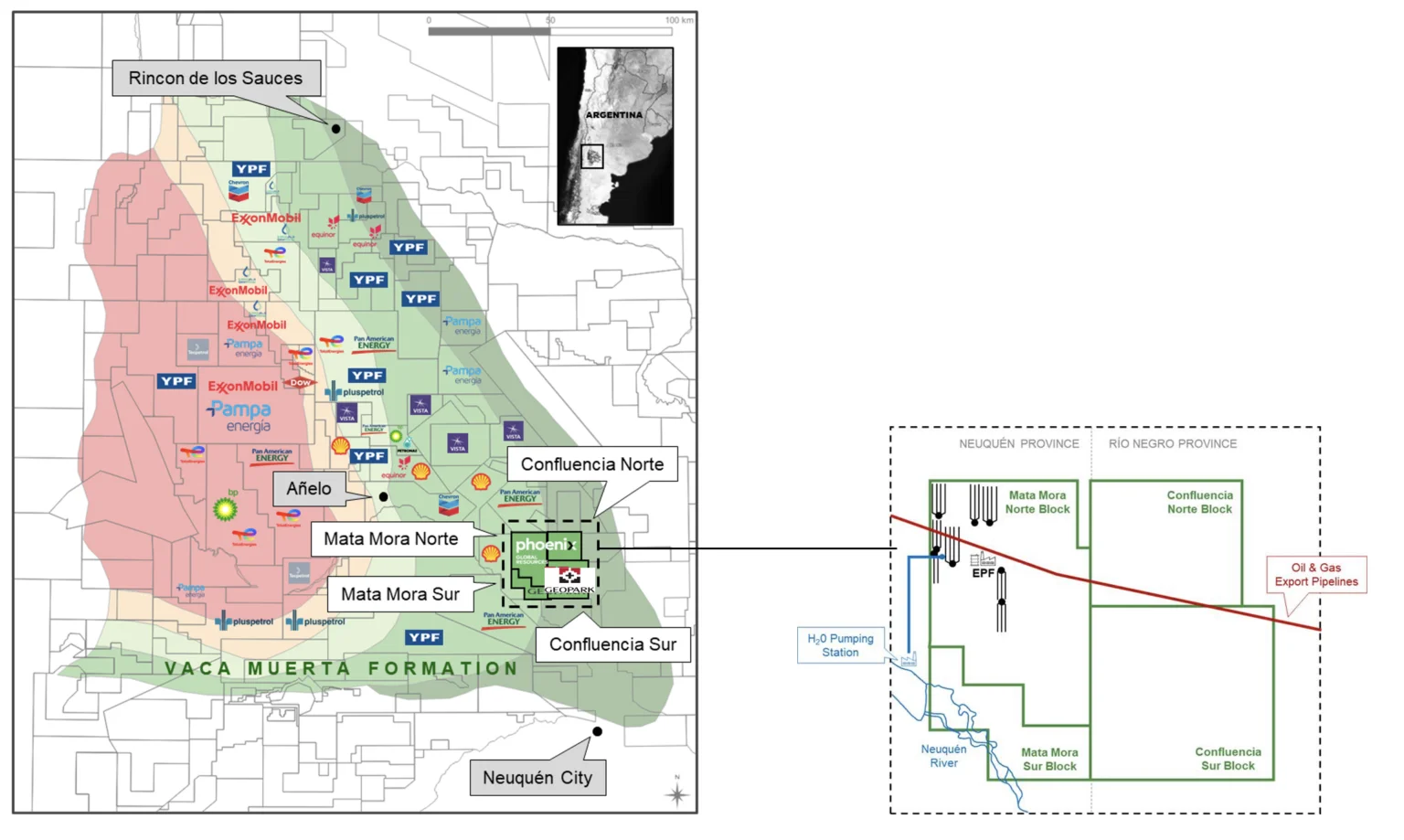

(GeoPark, 13.May.2024) — GeoPark Limited (NYSE: GPRK) signed an Asset Purchase Agreement with Phoenix Global Resources (PGR), a subsidiary of Mercuria Energy Trading, for the acquisition of non-operated working interest (WI) in four adjacent unconventional blocks in the Neuquén Basin in Argentina as follows: a 45% WI in each of the Mata Mora Norte producing block and Mata Mora Sur exploration block, located in Neuquén Province, and a 50% WI in each of the Confluencia Norte and Confluencia Sur exploration blocks, located in Rio Negro Province.

KEY HIGHLIGHTS

Robust Strategic Fit

- The Vaca Muerta shale formation is the best onshore hydrocarbons play in Latin America today. It holds an estimated 16 billion bbl of oil and 300+ Tcf of unconventional gas resources with less than 10% developed to date[1]

- Oil production from Vaca Muerta has grown almost 4x since 2019 to 352,715 bopd[2]. It is currently contributing 50% of Argentina’s total oil production, and has the potential to triple again over the next six years

- Vaca Muerta has been significantly de-risked since 2009, with the drilling of almost 7,000 exploration and development wells

- The blocks are located in the oil window of the Vaca Muerta formation in the Neuquen Basin, one hour from Neuquen city and close to the services hub. Immediately adjacent blocks currently produce over 28,000 gross boepd[3]

- GeoPark leverages more than 20 years of operational and business presence in Argentina

- Acquisition complements existing GeoPark portfolio assets in Colombia, Ecuador and Brazil

Immediate Access to Rapidly Growing Production Profile

- The new assets would increase GeoPark’s 2024 production by an estimated 5,500-6,500 net boepd, subject to when the closing date of the transaction occurs

- Average gross production of the assets was 11,220 boepd in 1Q2024[4] and 12,594 boepd in March 2024[5]

- Gross exit production for 2024 is expected to be between 13,500-14,000 boepd

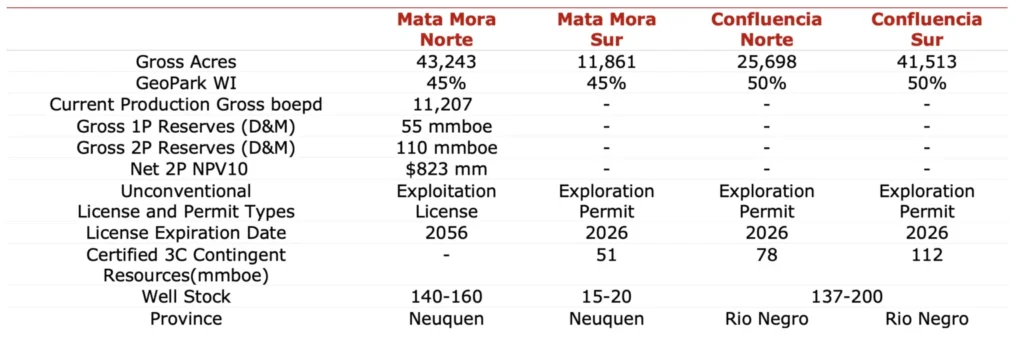

- Approximately 150 more gross drilling locations have been identified for the full development of the Mata Mora Norte Block

- Under the agreed indicative development program, production from the Mata Mora Norte Block is expected to reach approximately 40,000 gross boepd by 2028

Immediate Access to Rapidly Growing Reserves Profile

- The transaction represents access to 25 mmboe of 1P net reserves, 49.5 mmboe of 2P net reserves, and 102.6 mmboe of 3P net reserves, according to the Degolyer & MacNaughton (D&M) certification from December 2023

- GeoPark’s 1P Reserve Life Index (RLI) would grow to 6.7 years (from 5.4 years) and 2P Reserve Life Index (RLI) to 11.8 years (from 9.1 years) (D&M, December 2023)

Value Accretive from Day One

- The Mata Mora Norte Block is expected to generate net Adjusted EBITDA of $90mn-100mn[6] in full year 2024 with a 68% Adjusted EBITDA margin (at $80-90/bbl Brent oil price)

- At expected plateau production of 40,000 gross boepd in 2028-2030, the assets are expected to contribute $290mn-295mn of EBITDA to GeoPark (at $70/bbl Brent oil price)

- Net NPV10 of 1P Reserves is $364mn and net NPV10 of 2P reserves is $823mn[7]

Significant, Low-Risk Exploration Upside

- The Mata Mora Sur, Confluencia Norte and Confluencia Sur blocks are currently in the exploration phase and represent significant potential production and reserves upside

- The three exploration blocks have 79,000 gross acres and 241 mmboe of gross 3C certified Contingent resources (118 mmboe net to GeoPark)

- Exploration acreage is estimated to add 200 gross drilling locations

- Production from the exploration assets could reach 15,000 – 20,000 gross boepd by 2028 on a P50 basis, subject to exploration success

- First exploratory well on the Confluencia Norte Block is underway

Proven Partner & Operator

- PGR is an independent exploration and production (E&P) company focused on unconventional operations in Argentina. PGR is a subsidiary of Mercuria, one of the world’s leading independent energy and commodity groups, with more than $174bn of gross revenue and $6.7bn of equity in 2022

- PGR has grown production at Mata Mora Norte from zero to 13,000+ gross boepd in only three years, effectively de-risking 110 mmbbl of gross 2P reserves (D&M, December 2023)

- With robust design, Drilling & Completion (D&C) costs have fallen from $15.9 million per well in 2022 to $14.3mn per well in 2023, a highly competitive level compared to the major Vaca Muerta producers

- Lifting costs decreased from $8.10 per boe in 2022 to $5.80 per boe in 2023, and are expected to fall further to $5.10 per boe in 2024e (without transportation cost)

- The partnership between GeoPark and PGR represents an opportunity to jointly leverage the substantial operational, technical, financial and commercial expertise of both companies – underpinned by unique complementary entrepreneurial culture – to unlock the full potential of the acquired blocks

Summary of Terms

- GeoPark will pay $190mn for a total of 122,315 gross acres (58,402 net acres)

- In addition to the upfront consideration, GeoPark will fund 100% of exploratory commitments up to $113mn gross ($57mn of net carry), to be funded over two years, an acquisition of midstream capacity according to the WI of $11mn, and a $10mn bonus contingent on results in the Confluencia exploration campaign

- The transaction is expected to close before the end of 3Q2024, pending customary regulatory approvals

Competitive Valuation Metrics

- For Mata Mora Norte Block, the valuation is approximately $9,000 per acre[8]

- Based on net reserves, the valuations are $7.1/boe 1P reserves and $3.5/boe 2P reserves (D&M, December 2023)

- Valuation per flowing barrel at closing is approximately $28,000

- The 2024 EV/EBITDA multiple is 1.8x (at $80-90 Brent oil price)

- The plateau EV/EBITDA multiple is 0.6x (at $70 Brent oil price)

Financing and Capital Structure

- The upfront consideration will be funded with a mix of available cash and a partial draw of an existing oil prepayment facility that offers flexible and cost-effective terms. Longer term commitments will be funded with a combination of cash generated by the assets and financing

- The pro forma net debt to Adjusted EBITDA ratio following the transaction is not expected to exceed 1.1x[9]

Strategic Facilities and Infrastructure

- Facilities are in place to handle 20,000 boepd of gross production, and additional facilities will be in place by 2025-2026 to handle the expected plateau production

- Two oil pipelines run directly through the block and a third is under construction, facilitating transport options for exports

- Approximately 90% of oil sales are transported by pipeline, with 70% destined for export and 30% for the domestic market

- Gas production is approximately 6% of total production, with 50% sold to third parties and 50% used for internal consumption

Indicative Activity Plans

- The Mata Mora Norte Block currently has a dedicated drilling rig that is scheduled to drill 12-15 wells in 2024

- The full development and exploration plan for the Mata Mora Norte Block includes adding a second drilling rig in late 2025 to continue growing production to expected plateau levels, which include risked estimates of seven committed wells on two exploration blocks

Andrés Ocampo, Chief Executive Officer of GeoPark, said: “This transaction is transformational for GeoPark, adding immediate value-accretive production and reserves growth, while materially increasing and diversifying our long-term drilling inventory into one of the most prolific petroleum systems in the world. We are particularly encouraged by achieving this strategic step change alongside PGR, a proven and established operator with world class shareholders and great success in efficiently developing and de-risking the unconventional opportunities in Vaca Muerta.”

____________________