(CSI, 8.May.2019) — CSI Compressco LP today announced first quarter 2019 consolidated financial results and provided updated 2019 full year guidance.

Consolidated revenues for the quarter ended March 31, 2019 were $103 million compared to $138 million for the fourth quarter of 2018 and $85 million for the first quarter of 2018. Compared to the fourth quarter of 2018, total revenues decreased 25%, driven primarily by the timing of new equipment shipments and the completion of overhauls in aftermarket services. Compression services revenue and gross margins continued to increase sequentially. Net loss for the quarter ended March 31, 2019 was $12.5 million compared to a net loss of $3.7 million in the fourth quarter of 2018 and a net loss of $15.7 million in the first quarter of 2018.

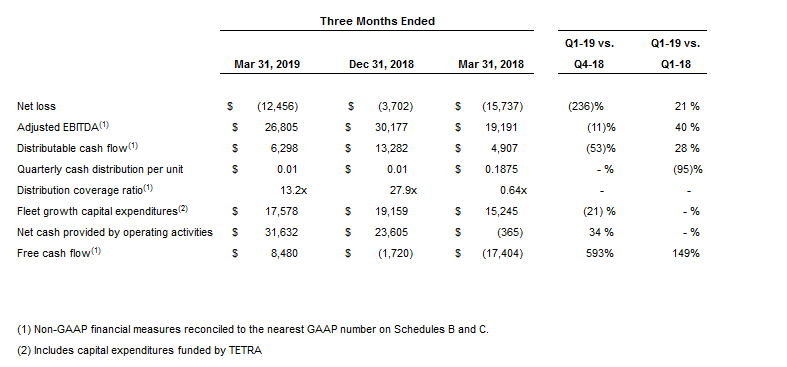

Selected key operational and financial metrics are as follows:

— First quarter 2019 Adjusted EBITDA(1) of $26.8 million decreased $3.4 million from $30.2 million in the fourth quarter of 2018 primarily due to lower new equipment sales, but was $7.6 million higher than in the first quarter of 2018.

— Compression services gross margins in the first quarter of 2019 improved 460 basis points (bps) to 48.2% from 43.6% in the fourth quarter of 2018, which included a $2.1 million non-income tax contingency. Excluding this charge in the fourth quarter of 2018, compression services gross margins improved 110 bps reflecting price increases, new units being deployed at higher rates and better cost controls(1).

— Overall service fleet utilization increased 60 bps compared to the end of the fourth quarter of 2018, to 87.2%. Utilization for large horsepower equipment, greater than 1,000 horsepower per unit, also increased 60 bps from the end of the fourth quarter, to 95.6%.

— Total operating fleet horsepower of 1,017,452 as of March 31, 2019 surpassed 1 million horsepower for the first time in the Company’s history.

— Backlog for new equipment sales was $93.9 million as of March 31, 2019, down from $105 million at the end of December 2018. New orders received in the first quarter 2019 were $11 million. As of May 8, 2019 new orders received were $14.7 million year-to-date.

— The coverage ratio on distributable cash flow(1) was 13.2X.

— The Company has continued to cash redeem the outstanding Series A Preferred Units. As of May 8, 2019 the outstanding balance is approximately $13.3 million.

(1) These measures are not presented in accordance with generally accepted accounting principles in the United States (“GAAP”). Please see Schedules B, C, D, and E for reconciliations of these non-GAAP financial measures to the most directly comparable GAAP measures.

Unaudited results of operations for the quarter ended March 31, 2019 compared to the prior quarter and the corresponding prior year quarter are presented in the accompanying financial tables.

Owen Serjeant, President of CSI Compressco, commented, “We are pleased with another good quarter driven by continued consistent and strong improvements in compression and related services. Although adjusted EBITDA was slightly behind the prior quarter’s results, this was due to the timing of new equipment shipments and aftermarket services major overhauls, both of which were at record highs in the fourth quarter of 2018. We had previously indicated that we expected the first quarter of 2019 to be sequentially weaker and are expecting the second quarter for both businesses to be materially higher than the first quarter due to the timing of shipments and completion of overhauls on our clients’ units. Compression and related services continues to get stronger each quarter and we’ve posted another sequential revenue and gross margin improvement. Market demand for compression and related services continues to be exceptionally strong. We have not seen any slowdown in this area. As new large horsepower units continue to be deployed, we see year over year spot price increase percentages in the high teens. The new equipment being deployed is achieving pricing above pricing on the existing units, allowing us to attain 65%-70% incremental fall through margins that are driving 20% returns on capital. We are focusing our investments in new units to our core customers, who are major operators in key shale basins that require more equipment to be deployed to their existing fields. These new units are addressing both gathering system requirements for the increasing volumes of associated gas and are also meeting their requirements for centralized gas lift. The need for centralized gas lift (utilizing multiple large horsepower compressors to service many wells drilled and producing in concentrated areas) continues to grow in support of initial early life oil production requirements and for enhanced oil recovery from those wells. Our aftermarket services and equipment sales businesses experienced a softer sequential quarter but were consistent with our internal expectations. First quarter bookings for new equipment sales were lower than prior quarters as customers have delayed committing to new orders. We expect the remainder of the year to be stronger for these two businesses as the identified opportunities remain strong. The pipeline of identified opportunities is in excess of $250 million. Second quarter revenue from new equipment shipments are expected to be significantly higher compared to $27 million in the first quarter 2019.

“We remain bullish on the overall compression space as the industry is one of the strongest in the oil and gas spectrum. Our customers are requesting significantly more equipment to address the increasing volumes of associated gas in the shale plays and to address the increasing need for centralized gas lift. We see the demand for compression equipment outpacing supply, especially for high horsepower equipment. We expect 2019 to be a strong year over year improvement across all business lines.

“We have a healthy backlog of $94 million for new equipment sales as of March 31, 2019 that will support our 2019 equipment sales expectations. Customer demand for high horsepower compression equipment in key basins remains strong and our key customers continue to invest in infrastructure that require large amounts of newbuild compression equipment. While some of our customers are taking a temporary pause from ordering new equipment to build out their infrastructure, we expect the rate of order intake to pick up substantially in the third and fourth quarters.

“New equipment orders were $11.2 million in the first quarter while total orders through May 7, 2019 are $14.7 million. Our new equipment quotation pipeline continues to get stronger and as the year progresses, we expect our order book to fill out to support our 2020 equipment sales.

“Compression and related services revenue was $63 million in the first quarter 2019 with gross margin of 48.2%, a 110 basis points improvement over the 47.1% in the fourth quarter 2018 excluding the non-income tax contingency charge of $2.1 million that was reflected in our fourth quarter of 2018 results (gross margin excluding the impact of the non-income tax contingency is a non-GAAP measure; see Schedule D for reconciliation of this non-GAAP financial measure). Compression and related services gross margin and utilization increased sequentially and we now have over 1 million active operating horsepower for the first time in the Partnership’s history. We are still seeing the benefit from better pricing as new equipment is added to the fleet, contracts roll over at higher prices, and as we add more equipment. We also continue to see operational efficiencies from our ERP system. In the first quarter of 2019 we deployed 38,983 of new horsepower to our service fleet, almost all exclusively in high horsepower equipment.

“As of March 31, 2019, aggregate compression and related services fleet horsepower totaled 1,167,164 and the overall fleet utilization rate was 87.2%, up 60 basis points from our exit utilization of 86.6% at December 31, 2018. Total operating fleet horsepower was 1,017,452 as of March 31, 2019 (we define the fleet utilization rate as the aggregate compressor package horsepower in service divided by the aggregate compressor package fleet horsepower as of such date). We do not exclude idle horsepower under repair or horsepower that is otherwise impaired from our calculation of utilization rates.

“Revenue from equipment sales was $26.8 million, a decrease of 52% from the fourth quarter, which had the highest quarterly sales since the acquisition of Compressor Systems, Inc. in 2014. We expect revenue from equipment sales to be significantly higher on a quarterly basis for the remainder of 2019.

“Aftermarket services revenue of $13.6 million was below the fourth quarter of 2018 levels due to the timing from the completion of major overhauls of our customer’s equipment. Based on our aftermarket order book, we believe this business will be much stronger the rest of the year and more in line with what we experienced in the second half of last year.

“We continue to make progress on cash redeeming the Series A Convertible Preferred Units. After May 8, 2019, the outstanding balance to be cash redeemed we will be approximately $14.0 million. Upon completion of the Series A Convertible Preferred Unit redemption, we expect to deploy approximately 50% of the increase in free cash flow towards growth capital opportunities targeting 20% returns from our key accounts. We remain committed towards improving our balance sheet and creating stakeholder value. Our goal remains to improve our leverage ratio to 4.5x, or better. Free cash flow not directed towards growth capital is expected to be used to either retire outstanding debt that will further improve our leverage metrics or will be returned to our unit-holders through the quarterly cash distributions. These decisions will be made as we continue to evaluate the prices that our units and bonds trade at and also on demand and pricing for new equipment opportunities. At the end of March, we did not have any amounts drawn on our asset based revolver. Total debt outstanding is $296 million on unsecured bonds and $350 million on secured bonds.”

Forward-Looking Guidance

We expect consolidated 2019 revenue to be between $490 million and $520 million and Adjusted EBITDA to be between $125 million and $140 million, consistent with our prior expectations. We further expect that our average distribution coverage ratio for 2019 will be between 30X and 35X at the end of 2019 with aggregate 2019 distributable cash flow to be between $55.5 million and $68.5 million. Reconciliations of expected adjusted EBITDA, distributable cash flow, free cash flow and distribution coverage ratio to the nearest GAAP financial measures are included on Schedule E.

We expect 2019 capital expenditures to total $60 million to $65 million, which we expect to fund from cash on hand and cash flow from operations. This range includes $18 million to $20 million for maintenance capital expenditures and $42 million to $45 million of growth capital expenditures that would add approximately 79,000 of horsepower to the fleet in 2019, all with client commitments. This range excludes $15 million, or 20,700 horsepower, that TETRA Technologies, Inc. (“TETRA”) agreed to purchase and lease to us under a five-year financing lease. However, for accounting purposes, the $15 million of fleet additions, funded by TETRA finance lease commitment, will be reflected as capital expenditures. We have the right to buy the equipment any time over the next five years in accordance with the terms of the agreements with TETRA, and have no obligation to buy the equipment at the end of the five-year term. This support from TETRA will allow us to meet current client demands without having to access the debt and equity markets or our credit facility.

Conference Call

CSI Compressco will host a conference call to discuss first quarter 2019 results today, May 8, 2019, at 10:30 a.m. Eastern Time. The phone number for the call is 1-866-374-8397. The conference will also be available by live audio webcast and may be accessed through CSI Compressco’s website at www.csicompressco.com. An audio replay of the conference call will be available at 1-877-344-7529, conference number 10127835, for one week following the conference call and the archived webcast call will be available through the Company’s website for 30 days following the conference call.

First Quarter 2019 Cash Distribution on Common Units

On April 18, 2019, CSI Compressco announced that the board of directors of its general partner declared a cash distribution attributable to the first quarter of 2019 of $0.01 per outstanding common unit, which will be paid on May 15, 2019, to common unitholders of record as of the close of business on May 1, 2019. The distribution coverage ratio (which is a non-GAAP Financial Measure defined and reconciled to the closest GAAP financial measure on Schedule B below) for the first quarter of 2019 was 13.2X.

CSI Compressco Overview

CSI Compressco is a provider of compression services and equipment for natural gas and oil production, gathering, transportation, processing, and storage. CSI Compressco’s compression and related services business includes a fleet of more than 5,700 compressor packages providing approximately 1.17 million in aggregate horsepower, utilizing a full spectrum of low, medium and high horsepower engines. CSI Compressco also provides well monitoring and automated sand separation services in conjunction with compression and related services in Mexico. CSI Compressco’s equipment sales business includes the fabrication and sale of standard compressor packages and custom-designed compressor packages designed and fabricated primarily at our facility in Midland, Texas. CSI Compressco’s aftermarket business provides compressor package reconfiguration and maintenance services, as well as the sale of compressor package parts and components manufactured by third-party suppliers. CSI Compressco’s customers comprise a broad base of natural gas and oil exploration and production, mid-stream, transmission, and storage companies operating throughout many of the onshore producing regions of the United States, as well as in a number of foreign countries, including Mexico, Canada and Argentina. CSI Compressco is managed by CSI Compressco GP Inc., which is an indirect, wholly owned subsidiary of TETRA Technologies, Inc. (NYSE: TTI).

***