(WoodMac, 30.Mar.2022) — Despite their scale, national oil companies (NOCs) have until now largely escaped the heavy scrutiny experienced by international oil companies (IOCs) around emissions. Partly as a consequence, the energy transition strategies of most NOCs significantly lag those of their leading IOC peers, says Wood Mackenzie, a Verisk business (Nasdaq:VRSK).

NOCs account for more than half of global oil and gas output, making them among the biggest global emitters of greenhouse gases. The 18 key NOCs covered in our report will produce 60 million barrels of oil equivalent per day (boe/d) in 2022; that compares to only 23 million boe/d for the Majors.

Wood Mackenzie research director Kavita Jadhav said: “As a result, NOCs will be responsible for half of forecast upstream direct (Scope 1 and 2) emissions between now and 2030. Also, that figure is expected to rise in future as NOCs exploit their high levels of remaining resource and available capital to seek significant production growth.”

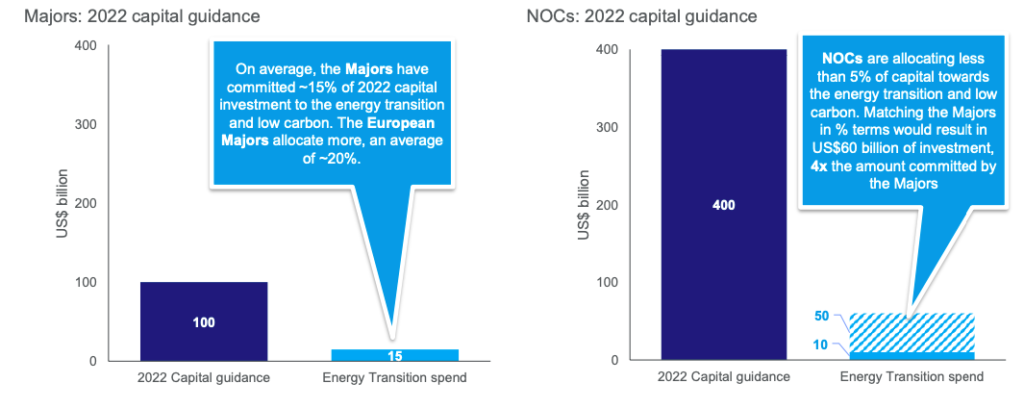

Despite the scale of their emissions, most NOCs are doing far less than their IOC peers to address the issue. NOCs have provided guidance which that indicates that they will spend four times the amount of capital that the Majors will spend in 2022. Out of this capital forecast, NOCs are currently committing less than 5% of capital to decarbonisation. In comparison, the Majors have allocated around 15% of 2022 capital investment to low-carbon projects, driven by regulatory, investor and public pressure. mounts. (The European Majors allocate more, at an average of around 20%.).

As intergovernmental pressure increases, NOCs will be pushed to follow the example set by the Majors. However, expect the pace of change to be slower, at least in the short term. With emissions reduction targets still mostly dictated by government and country-level climate goals, many NOCs have yet to make a net zero commitment.

NOCs lag the majors in committing capital towards the energy transition

Source: Wood Mackenzie Corporate Service; company announcements

Notes: Low carbon/energy transition capital guidance is provided by only a select few NOCs – PetroChina, Sinopec Corp, CNOOC Ltd, Rosneft, Petrobras, Ecopetrol, Pertamina, PTTEP and Petronas. Multi-year capital guidance has been annualised for 2022, based on Wood Mackenzie estimates.

Senior analyst Raphael Portela said: “There are strategies NOCs can take as they face the energy transition. Some NOCs could double down on their current approach. Middle East and Russian NOCs, in particular, have access to vast volumes of low-carbon oil and gas reserves, which could limit their exposure to future carbon costs. The largest resource holders currently continue to target production growth of 2-3% over the next decade. Those taking this approach set targets for emissions intensity, but not for absolute reduction, and decarbonisation or renewable projects remain at the planning stage.”

Other NOCs are harnessing their existing resource base to fuel a low-carbon transition. Some are targeting an increasing role for gas to support national decarbonisation goals, and allocating capital to, for example, carbon capture and storage (CCS) at the planning or pilot stage.

Finally, a few are taking the first steps to diversify into renewables and alternative energy projects that align with their existing portfolio strengths and corporate capabilities. NOCs with limited reserves who face a shorter remaining lifespan for their resources have a greater incentive to take this approach.

Portela said: “We are seeing NOCs targeting a range of low carbon opportunities, from electrification to CCS, biofuels, hydrogen and ammonia.”

Jadhav believes there are opportunities for NOCs to accelerate their energy transition strategies. Current high prices mean NOCs are set to generate a cash flow windfall of around US$110bn per year over the next five years. That will provide financial flexibility, and with it a golden opportunity to switch gears.

Jadhav said: “Sustained higher prices would allow NOCs to raise dividends and help service post-pandemic national debt at the same time as allocating capital to both upstream investment and low-carbon opportunities. If NOCs matched the Majors’ capital allocation to the energy transition the effects could be dramatic.

“For the Asian NOCs, higher oil and gas prices are now generating a wall of cash. We looked at what this means if prices stay higher for longer by using US$70/bbl versus our base case US$50/bbl. The result is the seven largest Asian NOCs generating an additional US$218bn of revenue through to 2030.”

____________________