(Frontera Energy Corporation, 3.Aug.2018) – Frontera Energy Corporation released its Interim Condensed Consolidated Financial Statements for the second quarter of 2018, together with its Management, Discussion and Analysis (MD&A). These documents will be posted on the Company’s website at www.fronteraenergy.ca and SEDAR at www.sedar.com. All values in this news release and the Company’s financial disclosures are in United States dollars unless otherwise stated.

SECOND QUARTER 2018 AND OTHER OPERATIONAL HIGHLIGHTS

Exploration and Development Update

— Acorazado-1 exploration well in the Llanos 25 block has reached total depth of 15,470 feet, a week ahead of schedule and under budget. Wireline logging operations are ongoing and depending upon results, testing is expected to be completed by the end of August.

— Delfin Sur-1 exploration well offshore Peru on Block Z-1 started drilling on July 14, 2018, is currently drilling at 6,000 feet and is expected to reach total depth by the middle of August.

— Alligator-4 development well in the Guatiquia block is producing at 1,370 bbl/d of 19.5 degree API oil.

Strong Financial Position and Results

— In July 2018, the Company exercised its right to terminate the Caño Limón (“CLC”) and Bicentenario (“BIC”) pipeline transportation agreements. As a consequence of these terminations, the Company is no longer committed to payments of ship-or-pay fees on these pipelines. As at June 30, 2018, these terminated contracts represented $1.36 billion in future transportation commitments.

— Separately Frontera reduced future transportation commitments on the Ocensa pipeline by over $178.3 million as a result of the successful settlement agreement in an arbitration on tariffs concerning the P-135 Project.

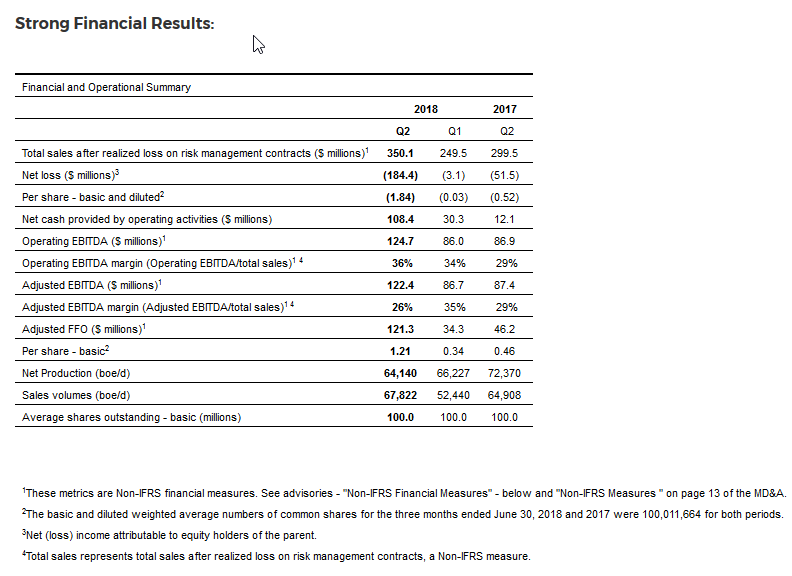

— The Company’s total cash position, including restricted cash, increased 5% quarter-over-quarter to $730.1 million at the end of Q2 2018.

— Total sales (after realized loss on risk management contracts) of $350.1 million were 40% higher than Q1 2018 and 17% higher than Q2 2017.

— The Company generated cash flow provided by operating activities of $108.4 million, an excess of $21.6 million above capital expenditures of $86.8 million.

— Net loss of $184.4 million, or $1.84/share, which includes an impairment of $107.7 million relating to the carrying value of the investment in Bicentenario, as a result of the termination of the BIC pipeline ship-or-pay agreement. This compares to a net loss of $3.1 million or $0.03/share, in the first quarter of 2018 and a net loss of $51.5 million or $0.52/share in the second quarter of 2017.

— Operating EBITDA of $124.7 million was 45% higher than Q1 2018 and 44% higher than Q2 2017.

— Operating Netback of $26.76/boe was 10% higher than Q1 2018 and 32% higher than Q2 2017.

— Adjusted FFO of $121.3 million was 254% higher than Q1 2018 and 163% higher than Q2 2017.

— The Company successfully completed an offering of $350 million senior unsecured notes at a coupon rate of 9.7%, due 2023 (“Senior Unsecured Notes”). Proceeds of the offering were used to repurchase its $250 million senior secured 10.0% coupon notes due 2021 (“Senior Secured Notes”) and for general corporate purposes.

— Implemented a Normal Course Issuer Bid (“NCIB”) for the repurchase of approximately 3.5% of the Company’s issued and outstanding common shares of which 33,100 shares were repurchased in July 2018 at a cost of $0.4 million.

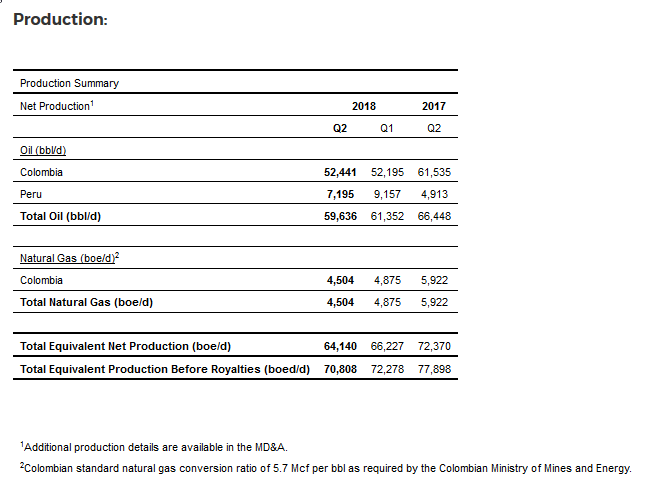

Production

— Net production decreased 3% quarter-over-quarter to 64,140 boe/d in Q2 2018 as a result of reduced production from Block 192 relating to a force majeure event on the NorPeruano pipeline in Peru and increased high-priced participation payment (“PAP”) royalty volumes at Quifa SW block in Colombia.

— The NorPeruano pipeline in Peru, which caused the force majeure event for production on Block 192 is expected to resume normal operations by the end of August.

— The Company completed the drilling of 24 development wells during Q2 2018, compared to 33 development wells and three exploration wells in Q1 2018.

— Total capital expenditure of $86.8 million during Q2 2018, were 10% higher than Q1 2018 as a result of spending related to exploration drilling of the Acorazado-1 exploration well on Llanos 25 block, preparation for the Delfin Sur-1 exploration well on Block Z-1 and the start of the water handling expansion project in the Quifa area.

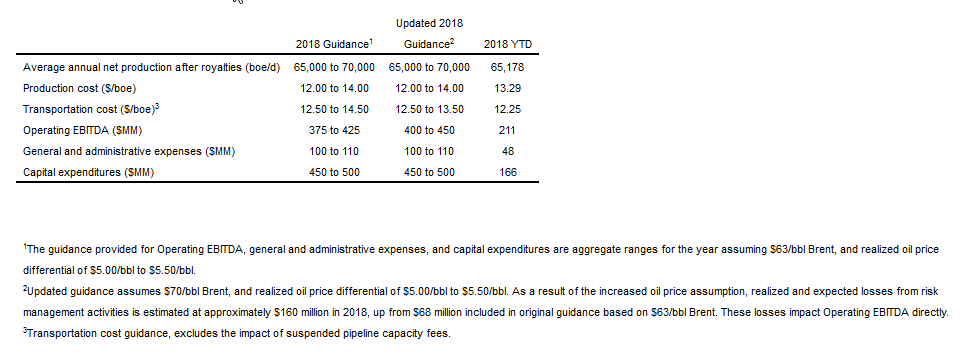

Updated 2018 Guidance

— The Company is increasing annual Operating EBITDA guidance by 6% at the midpoint to $400 to $450 million from $375 to $425 million and reiterates annual guidance for production of between 65,000 boe/d and 70,000 boe/d. This is in the context of year to date production of 65,178 boe/d which has been negatively impacted by third party events which include the force majeure event on the NorPeruano pipeline in Peru, increased PAP royalties at Quifa SW, and a now resolved community dispute on the Cubiro block.

Richard Herbert, Chief Executive Officer of Frontera, commented:

“Frontera had a very strong quarter. The recent terminations of our ship-or-pay contracts on the Caño Limón and Bicentenario pipelines will significantly reduce our future commitments by $1.36 billion and eliminate fees paid on suspended pipeline capacity. In 2017, suspended pipeline capacity fees totalled $122.5 million in addition to total company transportation costs of $346.3 million.

We successfully refinanced our secured $250 million, 10% coupon senior exit notes due in 2021 with unsecured $350 million, 9.7% coupon senior notes due in 2023. The refinancing provides the Company with additional capital as well as the increased financial flexibility needed to execute and deliver on our strategy and plans for 2019 and beyond. This flexibility has already enabled Frontera to execute a normal course issuer bid for 3.5% of the outstanding shares of the Company.

I am also pleased to report that we delivered strong financial results in the second quarter which generated nearly $125 million of Operating EBITDA and cash flow from operations in excess of capital expenditures. We are optimistic that improved operating efficiencies combined with continued strong international Brent oil prices will enable the Company to deliver strong financial results for the second half of 2018, which is reflected in our revised Operating EBITDA guidance. At Guatiquia we have had continued success on the Alligator field with the Alligator-4 well currently producing in excess of 1,300 bbl/d, in addition to the Alligator-3 well which is producing at over 1,400 bbl/d. We have drilled the Acorazado-1 exploration well ahead of schedule and under budget. We have also begun drilling the Delfin Sur-1 exploration well offshore Peru with results expected towards the end of August.”

Net production in the second quarter of 2018 totalled 64,140 boe/d, a decrease of 3% compared with the first quarter of 2018. The decrease in the quarterly production was primarily a result of reduced production from Block 192 in Peru due to the declaration of force majeure by Petroperu S.A. (“Petroperu”) on the NorPeruano pipeline which transports crude oil from Block 192 to the export terminal at Bayovar. Prior to the force majeure event, which suspended operations on June 4, 2018, the block was producing approximately 8,600 bbl/d net to Frontera. Petroperu began repairing the pipeline in mid-June with repairs expected in August. Upon reactivation of the pipeline, Frontera will commence pumping crude oil from storage and ramp production back up to pre-force majeure levels.

Production from Colombia remained stable during the quarter, with increasing production in the light and medium oil business unit offsetting reduced production in heavy oil, a result of higher PAP royalty volumes at Quifa SW. Positive production impacts included the resumption of normal operations from the Cubiro block during the second quarter and production from new exploration discoveries at the Alligator and Coralillo wells on the Guatiquia block which were connected to production facilities during the quarter. In addition, an intensive work-over campaign was conducted in June which has provided for the recovery of deferred production volumes for the remainder of 2018. These gains helped offset the impact of approximately 700 bbl/d of volumes lost as a result of PAP royalty volumes at Quifa SW.

During the second quarter of 2018, total capital expenditures were $86.8 million, 10% higher than $78.8 million in the previous quarter and 130% higher in comparison with $37.8 million in the second quarter of 2017. The increase during the second quarter relates to the initiation of drilling operations for the Acorazado-1 exploration well on the Llanos 25 block in Colombia, preparation relating to the drilling of the Delfin Sur-1 well offshore Peru on Block Z-1 and the start up of construction of additional water handling facilities in the Quifa area. Increased facilities spending in the quarter also connected the Alligator discoveries in the Guatiquia block to the main crude oil and water processing facilities on the block.

A total of 24 development and appraisal wells were drilled in the second quarter of 2018, in line with 25 wells planned. A number of development wells at Quifa SW originally planned for the first half of 2018 have been deferred to the second half of 2018 to match the start up of the increased water handling capacity project in the fourth quarter of 2018. The Company currently has nine drilling rigs operating, five in our Quifa SW heavy oil area, two at our Guatiquia light oil block, one on the Llanos 25 block and one on Block Z-1 offshore Peru. The Company expects to see a significant ramp-up of development well drilling from August until the end of the year. During the third quarter of 2018 the Company plans to drill 39 development wells and one exploration well. Over 32 development wells and two water injector wells are targeted to be drilled in the Quifa SW area.

Exploration and Development Update:

On July 23, the Acorazado-1 exploration well on the Llanos 25 block in Colombia reached total depth of 15,470 feet, a week ahead of schedule and under budget. Wireline logging activity used to evaluate and analyze the reservoir section is ongoing.

During the second quarter, the Company continued to have good results in the Alligator development in the Guatiquia block. Alligator-3 was drilled to a depth of 12,416 feet and started production on May 10, 2018 with an electrical submersible pump. During June 2018, the well produced at an average rate of 1,691 bbl/d, of 17.6 degree API crude with a 42% water cut and an average bottomhole pressure of 2,692 psi from the Lower Sand-1A reservoir.

On June 18, 2018, the Company began drilling the Alligator-4 development well on the Guatiquia block. On July 15, 2018, the well reached a total depth of 12,800 feet (12,315.4 feet TVD), encountering 12 feet of net pay in the Lower Sand-1A formation. The well was completed in the Lower Sand-1A formation with an electrical submersible pump. The Lower Sand-1A formation has been flow tested for three days at an average rate of 1,370 bbl/d of 19.5 degree API oil with an average water cut of 21% at stabilized bottom-hole flowing pressure with an approximate 21% drawdown. The well has produced a total of 3,368 bbls of oil over two days of testing.

The Company has received approval from its partner, Ecopetrol S.A. (“Ecopetrol”) to commence the long-term testing of the Jaspe-6D exploration well in the Quifa area that was initially drilled and tested in January 2018. This test is expected to allow the Company to move ahead with the drilling of two additional appraisal wells in late 2018, with the potential for declaring commerciality in early 2019.

The Company is in advanced discussions with its partner Ecopetrol in the Quifa SW block to implement a pilot multi-lateral horizontal development well program for 2019, with the expectation, that if successful drilling costs will be lower with resulting increased production and recovery rates.

In our offshore Peru operations in Block Z-1, mobilization of the Petrex-10 drilling rig was completed and the drilling of the Delfin Sur-1 exploration well began on July 14, 2018. The well is currently drilling at over 6,000 feet and is planned to be drilled to a total depth of 9,750 feet by the middle of August 2018.

The average Brent oil benchmark price increased by $7.74/bbl, or 12%, in the second quarter of 2018 to an average of $74.97/bbl, compared to $67.23/bbl in the first quarter of 2018. Brent oil benchmark price averaged $50.79/bbl in the second quarter of 2017. The Company’s realized oil price of $70.44/bbl in the second quarter of 2018 excludes the impact of $11.12/bbl of realized losses on risk management contracts. The Company remains hedged on approximately 60% of net daily production volumes until the end of October 2018 at an average ceiling price of $60.05/bbl compared to an average ceiling price received of $55.60/bbl in the first half of 2018. The Company is unhedged in November and December 2018.

For the second quarter of 2018, total sales after realized risk management contracts, increased 40% to $350.1 million compared to $249.5 million in the first quarter of 2018 and increased 17% from $299.5 million in the second quarter of 2017. Sales volumes were 6% higher than net production volumes as result of the 500,000 barrel benefit (approximately 5,500 bbl/d) from the oil cargo that was sold with crude oil inventory that had built up from prior periods. Sales in Peru decreased $24.3 million compared to the first quarter of 2018 as a cargo scheduled to load in June was not loaded until July. Oil sales in Peru continue despite the interrupted production on Block 192 as a result of a force majeure event. Historically, sales volumes trend between 3% and 5% below production volumes as a result of internal consumption.

During the second quarter of 2018, net loss attributable to equity holders of the Company was $184.4 million or $1.84/share, compared with a net loss of $3.1 million or $0.03/share, in the first quarter of 2018. The majority of the loss was attributable to an impairment of $107.7 million the Company recorded on its investment in Bicentenario, as a result of the termination of the BIC pipeline ship-or-pay agreement. In addition, other non-recurring losses included increased losses on realized risk management contracts of $26.2 million, a loss from the extinguishment of debt of $25.6 million and the reclassification of a currency translation adjustment relating to the sale of Petroelectrica de los Llanos of $50.8 million.

Operating EBITDA of $124.7 million or $1.25/share for the second quarter of 2018, was 45% higher in comparison with $86.0 million or $0.87/share achieved in the first quarter of 2018, and 44% higher than the second quarter of 2017, as a result of higher realized oil prices and higher sales volumes as noted above.

Adjusted FFO totalled $121.3 million or $1.21/share for the second quarter of 2018, an increase of 254% compared to $34.3 million or $0.34/share achieved in the first quarter of 2018, and 163% higher than the second quarter of 2017. The $87.0 million increase in adjusted FFO in the second quarter of 2018 was attributed to higher Operating EBITDA of $38.7 million and $48.4 million of dividends received from investments in associates ($0.0 million in the first quarter of 2018).

Strong Balance Sheet:

The Company continued to build cash during the quarter, with a total cash position of $730.1 million, as at June 30, 2018, an increase of 5% and 35% from the previous quarter and the second quarter of 2017, respectively. Unrestricted cash increased to $550.8 million as at June 30, 2018, from $515.8 million as at March 31, 2018. The increase in cash during the second quarter of 2018 was due to cash flow from operations in excess of capital expenditures and the refinancing of the Senior Secured Notes with Senior Unsecured Notes.

Working capital decreased 8% to $317.4 million during the second quarter of 2018, compared to $343.2 million at March 31, 2018.

The Company has reduced future transportation commitments in the Ocensa pipeline by over $178.3 million as a result of the successful settlement agreement in an arbitration on tariffs concerning the P-135 Project. Furthermore, the Company exercised its rights to terminate the CLC and BIC pipeline transportation agreements. As a consequence of these terminations, the Company is no longer contractually committed to payments of ship-or-pay fees on these pipelines. As at June 30, 2018, these terminated contracts represented $1.36 billion in future commitments.

The Company is hedged on approximately 60% of production between July and October 2018 with ceiling prices between $58.31/bbl and $61.83/bbl. Starting in November, the Company will be unhedged on 100% of production with current forward strip Brent oil prices in excess of $72/bbl.

In June 2018, as part of the refinancing of the Company’s Senior Secured Notes, Fitch Ratings Inc. assigned an initial rating of “B+/RR4” to the Company’s Senior Unsecured Notes, and maintained the “B+/Stable” Long Term Foreign Currency IRD. Standard & Poor’s assigned an initial rating of “BB-” to the Senior Unsecured Notes along with a reaffirmed Corporate Credit Rating of “BB-/Stable”.

The Company implemented an NCIB for the repurchase of approximately 3.5% of the Company’s issued and outstanding common shares of which 30,100 shares were repurchased in July 2018 at a cost of $0.4 million.

Annual Guidance Update:

The Company has increased its annual Operating EBITDA guidance by 6% at the midpoint to $400 to $450 million from $375 to $425 million as a result of increasing the Brent oil price assumption from $63/bbl to $70/bbl. As a result of the recent arbitration settlement on the P-135 Project pipeline tariffs combined with year to date results, the Company is narrowing the estimated range of transportation costs to $12.50/bbl to $13.50/bbl from $12.50/bbl to $14.50/bbl. Original 2018 Operating EBITDA guidance assumed uptime on the BIC pipeline of 50% in the first half of 2018 and the implementation of a revised ship or pay agreement in the second half of 2018. Guidance metrics for net production, production costs, general and administrative expenses and capital expenditures remain unchanged.

Frontera Energy Corporation is a Canadian public company and a leading explorer and producer of crude oil and natural gas, with operations focused in Latin America. The Company has a diversified portfolio of assets with interests in more than 30 exploration and production blocks in Colombia and Peru. The Company’s strategy is focused on sustainable growth in production and reserves.

***