(Frontera Energy, 7.Nov.2018) — Frontera Energy Corporation released its Interim Condensed Consolidated Financial Statements for the third quarter of 2018, together with its Management, Discussion and Analysis (MD&A).

These documents will be posted on the Company’s website at www.fronteraenergy.ca and SEDAR at www.sedar.com. All values in this news release and the Company’s financial disclosures are in United States dollars unless otherwise stated.

THIRD QUARTER 2018 OPERATIONAL AND FINANCIAL HIGHLIGHTS

— Cash provided by operating activities of $189.4 million in the third quarter generated $65.4 million of cash in excess of capital expenditures of $124.0 million and contributed to a total cash position of $786.5 million at quarter end. Cash and cash equivalents, unrestricted, increased 6% quarter-over-quarter to $586.6 million. Long term debt and obligations under finance lease were $352.3 million at quarter end.

— The Company has a significant cash position as well the opportunity to generate additional excess cash going forward. In addition to the existing normal course issuer bid (the “NCIB”) implemented by the Company during the third quarter, the Company will evaluate additional strategic initiatives designed to enhance shareholder returns.

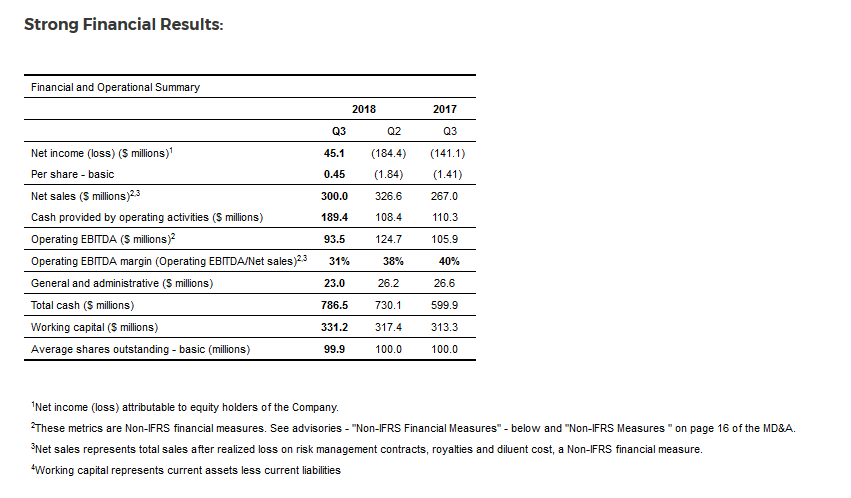

— Oil and gas sales and other revenue in the quarter of $382.2 million were up 38% from the prior year period and down 9% from the prior quarter. Net sales of $300.0 million increased 12% compared to the prior year period and were 8% lower than the second quarter of 2018.

— Net income of $45.1 million ($0.45/share) compared with a net loss of $141.1 million ($1.41/share) in the prior year period, and a net loss of $184.4 million ($1.84/share) in the prior quarter. Operating EBITDA of $93.5 million was down 12% from prior year period and 25% from the prior quarter. Operating Netback of $23.81/boe was 12% lower than the second quarter of 2018 and 2% higher than the third quarter of 2017.

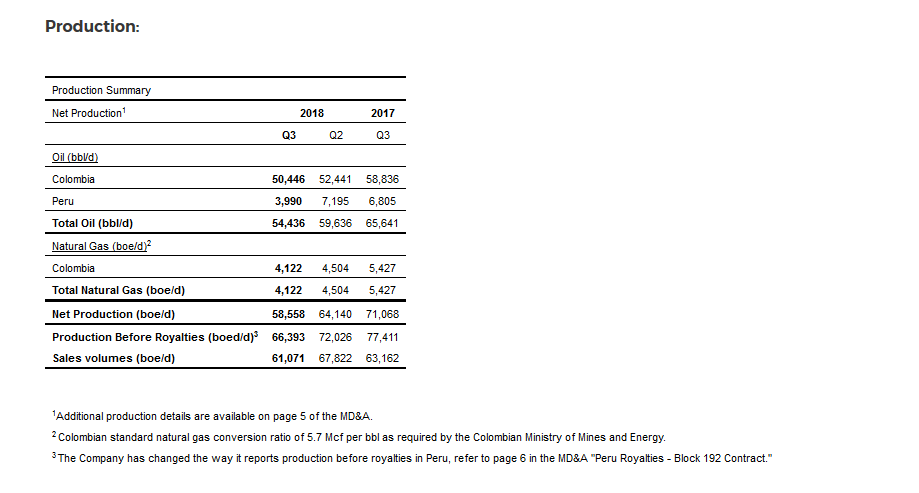

— Net production averaged 58,558 boe/d during the third quarter, down 18% and 9% from prior year period and prior quarter, respectively, reflecting a three-month suspension of production from Block 192 in Peru due to a force majeure event on the NorPeruano pipeline. This impacted quarterly production by approximately 5,700 bbl/d.

— Current net production is over 65,000 boe/d and is expected to grow throughout the fourth quarter. Production from Block 192, which restarted in early September, has consistently produced over 9,500 bbl/d since coming back on stream, reflecting the benefits of a work-over and well service program undertaken during the downtime. Production in Colombia is expected to increase in the fourth quarter, with the startup of the first phase of the water handling expansion project at Quifa SW on October 30, 2018, and the full 450,000 bbl/d increase in water handling capacity expected to be on stream by year end adding between 2,000 and 3,000 bbl/d of oil net to Frontera.

— The Company’s 2018 oil hedges, which capped the benefit of higher Brent oil prices through October 2018 (realized price after risk management contracts of $58.00/boe versus an average Brent oil benchmark price of $75.84/bbl during the third quarter), have now expired. The expiry of these hedge contracts is expected to have a positive impact on operating EBITDA and cash flow in the fourth quarter.

— General and administrative expenses of $23.0 million in the third quarter were 12% lower than the second quarter of 2018 and 14% lower than the third quarter of 2017 as the Company implements efficiency change projects throughout the organization.

— Substantial progress was achieved in managing long-term transportation costs during the quarter, with the termination of agreements representing a reduction in future commitments.

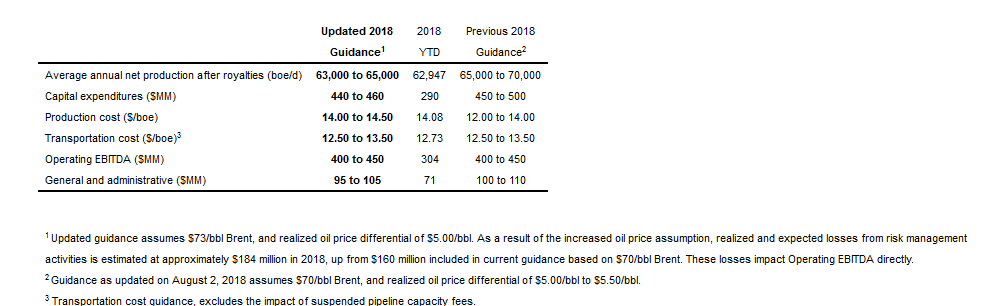

— The Company has maintained 2018 Operating EBITDA and transportation cost guidance while updating daily net production, capital expenditure, general and administrative expense and production cost guidance to reflect year to date results and expected results for the balance of the year.

Richard Herbert, Chief Executive Officer of Frontera, commented:

“Frontera performed well in the third quarter, generating significant cash flow and further strengthening our balance sheet, in spite of production interruptions. We also made good progress toward our 2018 and long-term goals for growth, efficiency and value creation. Going into the fourth quarter, I am encouraged by the resumption of production at Block 192 in Peru at higher levels, as a result of the service work we were able to accomplish during the pipeline suspension, and by growing production in Colombia from our drilling program as we ramp up activity and bring additional water handling capacity on-line.

We are also making progress securing Frontera’s growth with the discovery at Acorazado-1, our fourth exploration success in Colombia this year. Plans are well advanced to initiate a long-term test in the well before year-end. We have continued to accelerate our drilling activities within our existing portfolio. During the fourth quarter we expect to drill 36 wells, with 22 development wells at Quifa SW, seven water injection wells, two light and medium oil development wells on the Guatiquia block, two development wells at Zopilote Sur on the Cravo Viejo block and three exploration and appraisal wells.

We are excited by the opportunity of capturing higher oil prices after the expiration of our hedging contracts at the end of October. While a necessary risk management strategy during the Company’s restructuring in 2016, they have limited our ability to benefit from rising oil prices this year. Without a cap on our realized prices for the last two months of this year, we expect our exposure to Brent oil prices to increase by nearly $12 per barrel, based on recent prices, directly benefiting Frontera’s earnings and cash flow.

We are well positioned for 2019 with our strong cash position and balance sheet which will provide further opportunities for disciplined capital allocation into strategic growth projects and to enhance shareholder returns going forward.”

Gabriel de Alba, Chairman of the Board of Directors of the Company, said:

“The Frontera Board believes there are multiple opportunities to increase shareholder value. First, through a disciplined exploration and development investment plan together with initiatives to improve performance in order to support Frontera’s long-term free cash flow. Second, with Frontera trading at a significant discount to its asset value and relative to its peers, we are taking steps to close the valuation gap, including by enhancing trading liquidity. Last, we are actively evaluating additional strategic initiatives designed to enhance shareholder returns.”

Board of Directors Update:

The Company is announcing a number of changes to the composition of its Board of Directors. One of the Company’s Board members, Camilo Marulanda, has elected to resign from the Board as a result of increased demands since being named President of ISAGEN S.A. in Colombia. Mr. Marulanda will be replaced by Orlando Cabrales Segovia, a leader in the public and private energy sector in Colombia with over 30 years experience, including as Vice Minister of Energy of the Ministry of Mines and Energy in Colombia between 2013 and 2014 and as the President of the Agencia Nacional de Hidrocarburos (ANH) from 2011 to 2013. Mr. Cabrales held senior roles at BP in Latin America and has been on the Boards of numerous companies in Colombia including; ISAGEN S.A., Tuscany Drilling, Cenit Transporte y Logistica de Hidrocarburos S.A. (CENIT), and ISA. Mr. Cabrales earned an undergraduate degree in Law from Pontifical Javeriana University and a Masters degree in Philosophy from Boston College.

The Company is also pleased to announce the appointment of Veronique Giry to the Board of the Directors. With this appointment, the Company’s Board is back to seven members, all of whom are independent. Ms. Giry has an impressive track record in the global oil and gas industry and currently serves as Vice President and Chief Operating Officer of ISH Energy Limited in Calgary, Alberta, Canada. Ms. Giry’s 29 year career has included senior management roles at the Alberta Energy Regulator and Total Exploration & Production where she has held roles in Latin America, Canada, Asia, Europe and the UK. Ms. Giry earned a Masters in Engineering degree from Ecole Centrale de Paris, France, with a major in Mechanics and sits as a volunteer on the Board of Alliance Francaise of Calgary.

Mr. de Alba continued: “Frontera is excited to add Orlando’s and Veronique’s best-in-class regulatory and technical expertise to our Board of Directors. Their diverse operational knowledge and experience within the global upstream industry will be a significant benefit to the Company as we position for growth and cash flow generation. They will complement the skills of the other Board members. We would like to thank Camilo Marulanda for his valuable contribution to the Board over the past two years as we repositioned Frontera to be the leading publicly traded upstream oil and gas company in Latin America.”

The average Brent oil benchmark price increased by $0.87/bbl, or 1%, in the third quarter of 2018 to an average of $75.84/bbl, compared to $74.97/bbl in the second quarter of 2018. Brent oil benchmark price averaged $52.17/bbl in the third quarter of 2017. The Company’s realized oil price of $70.87/bbl in the third quarter of 2018 excludes the impact of $10.02/bbl of realized losses on risk management contracts. The Company had hedges in place for October 2018 on 1.2 million barrels of oil at an average Brent price of $59.22/bbl. The Company is unhedged in November and December 2018.

During the third quarter of 2018, net income attributable to equity holders of the Company was $45.1 million or $0.45/share, compared with a net loss of $184.4 million or $1.84/share, in the second quarter of 2018. Higher net income was mainly attributable to a reduction in fees paid on suspended pipeline capacity, a reversal of provision of high price clause, a reduction in depletion, depreciation and amortization, a reduction in general and administrative expenses, and the recognition of a deferred tax asset offset by an increase in oil and gas operating costs and impairments on assets and investments in associates.

For the third quarter of 2018, net sales of $300.0 million were 8% lower than $326.6 million in the second quarter of 2018 and 12% higher than $267.0 million the third quarter of 2017.

Cash provided by operating activities of $189.4 million for the third quarter was 75% higher than in the second quarter of 2018 as a result of strong operating netbacks combined with timing benefits within the cash management process. The Company generated $65.4 million of excess cash in the quarter as cash provided by operating activities of $189.4 million exceeded capital expenditures of $124.0 million.

Operating EBITDA of $93.5 million in the third quarter of 2018 was 25% lower in comparison with $124.7 million achieved in the second quarter of 2018, and 12% lower than $105.9 million in the third quarter of 2017, as a result of lower oil and gas sales volumes and higher oil and gas operating costs in the current period, partially driven by inflation linked to higher oil prices.

Frontera continues to focus on improving its cost structure and recently completed a project to increase organizational efficiency and reduce costs. This focus on cost helped the Company deliver lower general and administrative expenses of $23.0 million in the third quarter of 2018, a decrease of 12% from the second quarter of 2018, and a decrease of 14% from the third quarter of 2017. Going forward, the Company will look to further improve operational efficiency to drive additional cost savings.

Strong Balance Sheet:

The Company continued to build cash during the quarter, with a total cash position of $786.5 million, as of September 30, 2018, an increase of 8% and 31% from the end of the second quarter of 2018 and of the third quarter of 2017, respectively. Unrestricted cash increased to $586.6 million as at September 30, 2018, from $550.8 million as at June 30, 2018. The increase in unrestricted cash during the third quarter of 2018 was due to cash flow from operations in excess of capital expenditures, offset by an increase in restricted cash and share repurchases. In October 2018, $45 million of restricted cash became unrestricted following the satisfaction of terms relating to the sale of Petroelectrica de los Llanos.

Working capital, or current assets less current liabilities, increased 4% to $331.2 million during the third quarter of 2018, compared to $317.4 million at June 30, 2018.

The Company has hedged 1.9 million barrels of production between January 2019 and September 2019 using a Brent put price of $55/bbl, which protects the Company from lower oil prices while retaining the upside from potentially higher oil prices.

On October 4, 2018, S&P Global Ratings reaffirmed its ‘BB-’ global scale long-term issuer credit rating on the Company and its ‘BB-’ issue-level rating on the Company’s $350 million senior unsecured notes due 2023.

During the third quarter of 2018 the Toronto Stock Exchange (TSX) accepted the Company’s notice of intention to initiate a NCIB for its common shares. The notice provides that Frontera may purchase, during the twelve-month period commencing July 18, 2018 and ending July 17, 2019, up to 3,543,270 Common Shares, representing approximately 3.5% of the Company’s 100,011,664 issued and outstanding Common Shares as at July 9, 2018. Under the Company’s NCIB 315,512 shares were repurchased for cancellation at a cost of $4.5 million (C$18.68 per share) during the third quarter of 2018. Subsequent to September 30, 2018, a further 165,049 shares were repurchased at a cost of $2.2 million (C$17.49 per share).

The NCIB, in addition to the two for one stock split undertaken earlier in 2018 has helped improve the average daily trading volume in the Company’s equity by over three times compared to what it was at the beginning of 2018.

Update on Transportation Costs:

On July 13, 2018 the Company announced the successful settlement of the Ocensa transportation arbitration concerning the P-135 Project. As a result, the Company has reduced future transportation commitments in the Ocensa pipeline by over $178.3 million during the life of the contracts (June 2017 through June 2025). The Company also announced that it had terminated its contractual commitment with CENIT to transport oil through the Caño Limón-Coveñas pipeline (CLC) and its contractual commitment with Oleoducto Bicentenario de Colombia S.A.S. to transport oil through the Bicentenario pipeline (“BIC”). As a consequence of these terminations, the Company is no longer contractually committed to payments of ship-or-pay fees on these pipelines; these terminated contracts represented $1.36 billion in future transportation commitments through to October 2028.

During the third quarter of 2018, the Company realized $5.6 million of fees paid on suspended pipeline capacity, for the period between July 1 and July 12, 2018 before the contracts were terminated. These costs are excluded from the Company’s transportation costs, consistent with their historical reporting. A further third quarter charge of $15.6 million was taken for prepayments and standby letters of credit (“SBLCs”) on the BIC pipeline, representing (i) $5.3 million of SBLCs which were drawn by Bicentenario and (ii) a further $10.3 million of prepayments to Bicentenario and accounts receivables by the Company related to the Bicentenario transportation contracts. Under the Company’s unsecured letter of credit facility, a total of $64.4 million of SBLCs were issued relating to the Company’s transportation contract with Bicentenario. The remaining $59.1 million were drawn after the end of the third quarter and will be recognized as an expense in the fourth quarter of 2018. The Company has reimbursed issuing banks the full amount drawn under the Bicentenario SBLCs. The Company is of the view that the drawdown of the SBLCs was wrongful and is evaluating its remedies with respect thereto.

The Company has alternative transportation agreements in place which provide sufficient capacity for the evacuation and sale of its oil production in Colombia.

Current net production is over 65,000 boe/d and is expected to continue to increase during the fourth quarter as the Quifa SW water handling expansion project comes on stream. Net production in the third quarter of 2018 averaged 58,558 boe/d, a decrease of 9% compared with the second quarter of 2018. The decrease in quarterly net production was a result of a suspension of production from Block 192 in Peru due to the declaration of force majeure by Petroperu S.A. on the NorPeruano pipeline which transports crude oil from Block 192 to the export terminal at Bayovar. The pipeline was out of service between June 4, 2018 and August 30, 2018 when it was restarted. Since the pipeline was restarted, average net production has been approximately 9,500 bbl/d or 12% higher than before the force majeure event, reflecting benefits from work-over and other maintenance activities which were undertaken while production was suspended.

Production from Colombia decreased 4% during the third quarter of 2018 compared with the previous quarter, as a result of temporary water injection restrictions encountered on the Casimena block, and natural production declines in the Company’s natural gas assets in the country.

Sales volumes for the three months ended September 30, 2018, were lower than the comparable prior year period primarily due to lower production in Colombia and higher inventory in Peru, resulting in lower volumes available for sale. During the third quarter of 2018, the Company sold more barrels than it produced in Colombia, resulting in an overlift liability position of 809 Mbbl at the end of the quarter.

During the third quarter of 2018, total capital expenditures were $124.0 million, 43% higher than $86.8 million in the previous quarter and 155% higher in comparison with $48.6 million in the third quarter of 2017. The increase during the third quarter relates to drilling operations for the Acorazado-1 exploration well on the Llanos 25 block in Colombia, the drilling of the Delfin Sur-1 well offshore Peru on block Z-1, and the start up of construction of additional water handling facilities in the Quifa area. Increased facilities spending in the quarter also connected the Alligator discoveries in the Guatiquia block to the main crude oil and water processing facilities on the block.

A total of 39 wells were drilled in the third quarter of 2018, in line with 40 wells planned. Thirty-one heavy oil development wells and two water injection wells were drilled in the Quifa SW area in connection with the increased fluid handling capacity that is expected to come on stream in the fourth quarter. Three light oil development wells were drilled on the Guatiquia block, two at Avispa and one at Alligator. A second Alligator well, Alligator-5, encountered the edge of the field and was uneconomic. The Company also completed the drilling of two exploration wells, the Acorazado-1 well on the Llanos 25 block onshore Colombia and the Delfin Sur-1 well on block Z-1 offshore Peru, the results of which have been previously disclosed.

During the fourth quarter of 2018, the Company plans to drill 36 wells including 22 development wells in the Quifa SW area, four development wells in its light and medium oil areas, three exploration wells, five water injection wells at Orito and Neiva, and two water injection wells in the Quifa SW area. The Company will keep 10 rigs active throughout the fourth quarter.

Exploration and Development Update:

On October 30, 2018 the Company started the commissioning of the water handling expansion project at the Quifa SW block. The project is expected to add approximately 450,000 bbl/d of new water handling capacity or a 40% increase to the current capacity. The Company plans to start the project in phases throughout the fourth quarter with full capacity on stream by the end of the year. The increased water handling capacity is expected to be able to deliver between 2,000 and 3,000 bbl/d of incremental net production by year end.

During the fourth quarter of 2018, the Company plans to drill three exploration wells compared to the prior plan of five wells: the Coralillo-3 well on the Guatiquia block which follows on from the successful Coralillo-1 well drilled and completed earlier in the year; the Chaman-2D commitment well on the Sabanero block; and the Jaspe-7D well in the Jaspe field within the Quifa area, a follow up to the successful Jaspe-6D well drilled in January 2018. The Cocodrillo-1 and Jaspe-8D wells will now be drilled in the first half of 2019 as a result of permitting delays.

The Company will commence the expansion of the waterflood pressure maintenance project in the Neiva field by drilling six water injector wells in the fourth quarter. Upon completion of the drilling of the injector wells it is expected that pressure response and increased production will be encountered in the following six to twelve months. The expansion of the Neiva waterflood project will be the second pressure maintenance project to be implemented at Frontera post restructuring, following the pressure maintenance project at the Company’s Copa field in the Cubiro block.

The Company continues to drill additional development wells in various blocks identified by ongoing technical reviews of its assets. In June 2018, the ANH granted an extension of acreage to the Cravo Viejo block allowing the Company to capture additional acreage containing a mapped extension to the Zopilote field. This additional acreage has allowed the Company to commence the drilling of Zopilote Sur-1, to be followed by Zopilote Sur-2 subject to ANH approval. Additionally, the Company will drill two development wells on the Candelilla field in the Guatiquia block following the identification of separate Lower Sand-1 and Guadalupe formation opportunities which were previously thought not to be present. The Company was also recently successful in drilling a well in the Alligator field to more than 12,000 feet using only two casing strings. This new well design will now be used in certain future development wells, thereby contributing to a reduction in overall drilling costs.

The Company has received approval from its partner Ecopetrol to commence the long-term testing of the Jaspe-6D exploration well in the Quifa area that was initially drilled and tested in January 2018. The results of the test will provide the information required to evaluate the declaration of commerciality in 2019. The Company has secured approval from Ecopetrol to commence a cost cutting pilot drilling program in the Quifa field, which if successful will permit the drilling of the future horizontal development wells in a more cost-effective manner.

The Company is in advanced discussions with Ecopetrol in the Quifa SW block to implement a pilot multi-lateral horizontal development well program for 2019, with the expectation that, if successful, drilling costs will be lower with resulting increased production and recovery rates.

Annual Guidance Update:

The Company is affirming 2018 Operating EBITDA guidance of $400 to $450 million, and transportation costs per boe, while updating its annual guidance for net production, capital expenditures and production costs to reflect year-to-date results. The midpoint of average annual daily net production guidance is lowered by 5% to 64,000 boe/d (from 67,500 boe/d) with a corresponding 5% decrease to the midpoint of capital expenditures guidance to $450 million (from $475 million). Production cost guidance is increased to a midpoint value of $14.25/boe (from $13.00/boe), to reflect lower daily production volumes and inflationary pressures due to higher oil prices. General and administrative cost guidance for the year was decreased by 5% to a midpoint of $100 million (from $105 million), to reflect the benefit of recent cost savings initiatives. The guidance reflects an assumed average annual oil price of $73/bbl Brent (4% increase) and a realized oil price differential of $5 bbl (5% decrease).

Third Quarter 2018 Conference Call Details:

As previously disclosed, a conference call for investors and analysts is scheduled for Thursday, November 8, 2018 at 8:00 a.m. (MST) and 10:00 a.m. (EST,GMT-5). Participants will include Gabriel de Alba, Chairman of the Board of Directors, Richard Herbert, Chief Executive Officer, David Dyck, Chief Financial Officer and select members of the senior management team.

A presentation and webcast link will be available on the Company’s website prior to the call, which can be accessed at www.fronteraenergy.ca.

Analysts and interested investors are invited to participate using the following dial-in numbers:

| Participant Number (International/Local): | (647) 427-7450 |

| Participant Number (Toll free Colombia): | 01-800-518-0661 |

| Participant Number (Toll free North America): | (888) 231-8191 |

| Conference ID: | 4789788 |

| Webcast: | www.fronteraenergy.ca |

A replay of the conference call will be available until 11:59 p.m. (EST, GMT-5), Thursday, November 22, 2018 and can be accessed using the following dial-in numbers:

| Encore Toll Free Dial-in Number: | 1-855-859-2056 |

| Local Dial-in-Number: | (416)-849-0833 |

| Encore ID: | 4789788 |

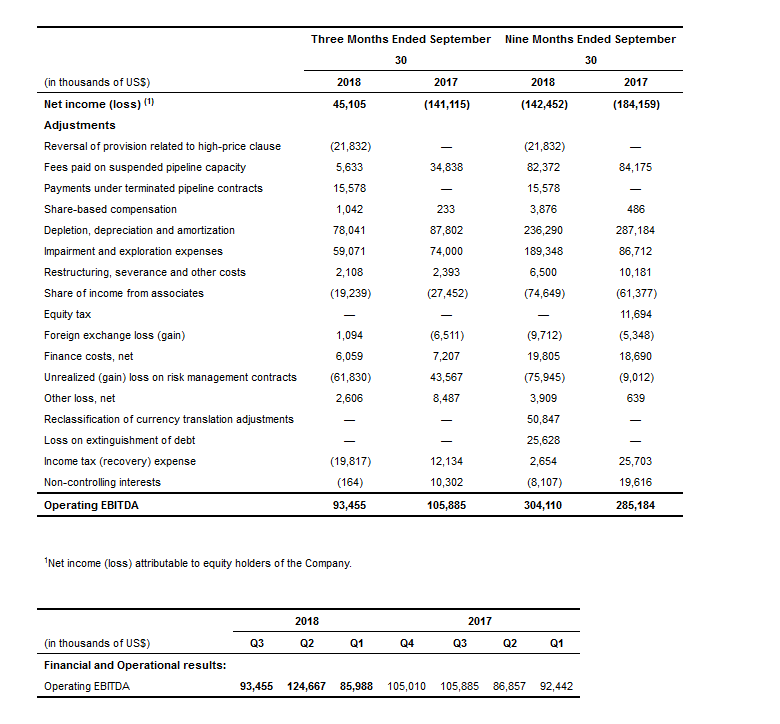

The following table provides a complete reconciliation of net income (loss) to operating EBITDA:

—————-

***

#LatAmNRG